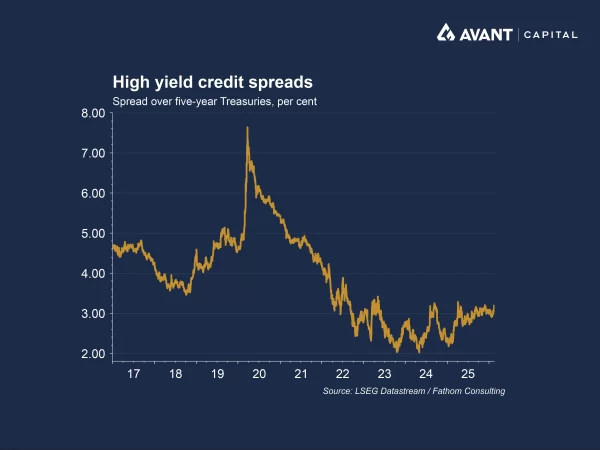

A surge in the corporate bond rally has driven spreads to their tightest levels in decades, sparking concerns that investors may be underestimating risk. With yields compressed and demand for debt at record highs, the question is no longer whether opportunities exist, but whether the reward still justifies the risk.

Why does yield compression create asymmetric downside?

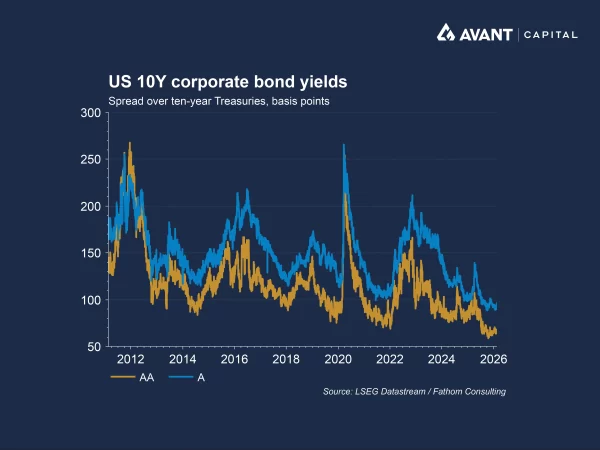

When spreads are this tight, the margin for error shrinks dramatically. Analysts at Citi warn that “the compression at the top creates significant asymmetric risk; the consequences of a market shock are now much higher” [2]. The gap between A and AA-rated bonds has fallen below 0.2%, while the difference between BBB and A-rated debt is just above 0.3%, near historic lows [2]. A sudden repricing, triggered by economic weakness, policy shifts, or a liquidity squeeze, could see spreads widen sharply as perceived default risks and credit default swap (CDS) costs increase, inflicting losses on portfolios that chased yield without regard for risk.

The total yield on US investment-grade corporate bonds remains close to 5%, supported by higher government bond yields since the pandemic [2]. But that headline number masks the reality: most of the yield comes from sovereign rates, not credit spreads. If government yields fall in a downturn, credit spreads could widen at the same time, creating a double hit for investors overweight in long-duration credit.

How does quality dilution and issuer leverage add to vulnerability?

The second risk lies in the quality of issuance. Companies are seizing the moment to lock in cheap funding, and not all of them are fortress balance sheets. Alphabet recently issued a rare 100-year bond, while Oracle tapped the market for US$25 billion despite concerns about rising leverage linked to AI investment [2]. Lower-rated issuers are also active, with double B-rated names pricing aggressively. While this does not signal imminent defaults, it does mean investors are being paid less to hold more leveraged credit, a dynamic that rarely ends well when growth slows.

Fund managers are responding by rotating up in quality. Phoenix Group, a major institutional investor, has trimmed corporate debt exposure and shifted into gilts, citing bubble-like behaviour emerging in parts of the credit market, particularly across lower-quality segments [2]. This move underscores a broader theme: in a market where spreads no longer compensate for risk, selectivity becomes paramount.

Could liquidity disappear when conditions change?

The third risk is liquidity. In good times, oversubscribed deals and record inflows create an illusion of depth. Weekly US investment-grade supply has reached multi-year highs, almost double expectations, and deals have been heavily oversubscribed. But history shows that when sentiment turns, liquidity in corporate credit can evaporate quickly. The post-2008 regulatory environment has reduced dealer balance sheet capacity, meaning secondary market support is thinner than it once was. If spreads gap wider, investors relying on quick exits may find themselves trapped.

This is why some managers describe today’s environment as a “bond picker market.” Broad beta exposure is unlikely to deliver the same tailwinds as in 2023 to 2025. Instead, portfolios need to be constructed with an eye on resilience, focusing on issuers with strong fundamentals, manageable leverage, and predictable cash flows.

What this means for investors

The corporate bond rally reflects powerful technical forces, but it also embeds risks that cannot be ignored. Compressed spreads, quality dilution, and liquidity fragility all point to a market where caution is warranted. For investors, the challenge is not to avoid credit altogether, but to approach it with discipline: understand what you own, why you own it, and how it behaves under stress.

In an environment where yield is scarce and risk is mispriced, the winners will be those who prioritise quality and liquidity over incremental basis points. The rally may continue, but when the turn comes, it will not be forgiving.

References

[2] https://www.ft.com/content/e87f04d5-9a19-4776-b0bc-3a78770be894