The latest turbulence across private credit markets has raised concerns among investors who have grown accustomed to years of rapid inflows, steady returns and the promise of insulation from public‑market volatility. Recent developments at firms such as KKR and Blue Owl, alongside mounting strains in private equity portfolios, particularly in software, suggest the industry could be confronting a critical inflection point. Understanding why these pressures have emerged, and what they may signal, requires looking at the convergence of rising defaults, stretched deal valuations, and technology‑driven disruption.

Why have private credit funds like KKR’s FSK been hit with steep markdowns?

The sharp markdowns within KKR’s FS KKR Capital Corporation (FSK) reflect growing stress across loans to private‑equity‑backed mid‑sized companies. FSK, which oversees a US$13bn loan portfolio, endured a 15 per cent share price drop after reporting a jump in troubled loans, reduced investment income and a dividend cut1. The fund’s valuation decline has been closely tied to its exposure to software companies, an area that was heavily financed during the private equity boom of 2021–2022, a period marked by ultra‑low interest rates and aggressive buyout activity. Software‑linked loans, along with exposures to janitorial services, veterinary roll-ups and dental groups, saw some of the most significant markdowns.

A striking example is FSK’s write‑down of loans tied to Medallia, the customer service software company acquired by Thoma Bravo for US$6.4bn in 2022, which were marked to below 80 cents on the dollar. Other business development companies made similar reductions on the same loans, underscoring that the weakness is not fund‑specific but industry‑wide.

How has Blue Owl become a flashpoint for the private credit industry?

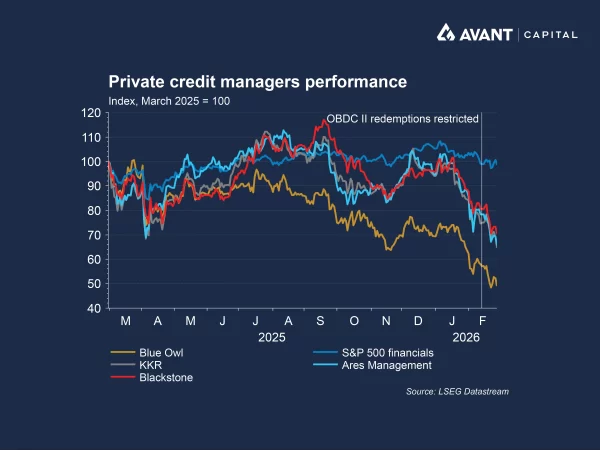

Blue Owl’s recent actions have heightened concerns around liquidity and valuations in private credit, while also contributing to a widening in high‑yield credit spreads. The firm’s decision to permanently restrict redemptions at its retail‑focused vehicle, Blue Owl Capital Corp II (OBDC II), triggered a sharp sell‑off across listed private capital managers and sent ripples through the broader sector2. Shares of major players, including Blue Owl, KKR, Blackstone and Ares, fell as investors reassessed the risks embedded in credit funds offering periodic liquidity despite holding illiquid assets.

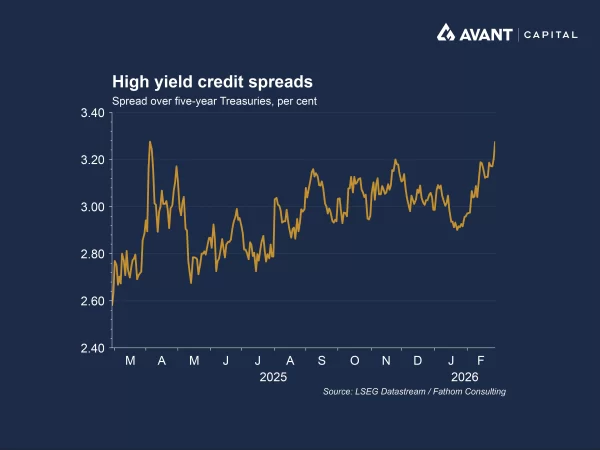

The move to halt withdrawals did not occur in a vacuum. OBDC II faced accelerating redemption requests in late 2025 as investors questioned the valuations of its software‑heavy portfolio. A previous attempt to merge the fund with a larger listed vehicle, one trading at a meaningful discount to net asset value, had already alarmed investors who would have been forced to crystallise losses. The subsequent permanent halt to withdrawals, combined with a sale of US$600mn of loans at roughly par value, was designed to stabilise confidence but instead deepened concerns about the integrity of marks and the liquidity structure of retail‑oriented credit funds. Yet despite these stresses, investment‑grade credit spreads have remained tight, underscoring continued investor confidence in higher‑quality issuers and signalling that concerns are concentrated in the riskier parts of the market rather than the broader credit spectrum.

Despite Blue Owl’s insistence that credit quality remains strong, with defaults low and software representing only a minor share of total assets, redemptions have continued to rise across its funds. Its Technology Income Corp vehicle saw investors pull more than 15 per cent of net assets in January, while its Credit Income Fund encountered US$1bn in withdrawals in late 20253. The episode has become a touchstone for the industry’s broader vulnerability to confidence shocks.

What is driving pressure across private markets, and why is software at the centre?

The private equity industry is facing its own parallel challenges, closely intertwined with private credit stress. After a decade in which software became the single biggest category of private equity dealmaking, representing up to 40 per cent of global activity, the sector is undergoing a significant repricing4. Many of the largest software buyouts were completed at peak valuations during 2020–2022, financed with substantial debt and premised on continued growth. Those assumptions are now in question.

The rise of AI has triggered a widespread reassessment of the business models underpinning specialist software firms. Leading AI models have accelerated fears that core functions, from customer service to analytics, could be automated at lower cost, threatening revenue growth for companies that were acquired at steep multiples. Public software stocks have fallen by more than a fifth in recent months, and investor anxiety has spilled into private markets, placing pressure on highly leveraged portfolio companies and the lenders that financed them.

As a result, private equity groups have slowed exits and are sitting on nearly US$4tn in unsold deals, tightening liquidity across the system. In many cases, valuations implied by public market comparables have dropped by more than two‑thirds, leaving investors exposed.

What do these developments signal for investors?

Together, the pressures facing KKR, Blue Owl and software‑exposed private equity portfolios point to a shift into a phase where valuation accuracy and transparency matter far more than they did during the boom years. The traditional appeals of private credit, steady income, and distance from public‑market volatility, are being challenged as liquidity strains emerge and technology disrupts key underlying sectors.

For investors, the lesson is not that private credit or private equity is fundamentally broken, but that the cycle has clearly turned. Transparency around valuations, risk within portfolios and the resilience of liquidity frameworks will likely remain key points of scrutiny in the months ahead.

References

- Financial Times, “Private credit fund managed by KKR reports jump in troubled loans,” 27 February 2026

- Financial Times, “Private credit stocks slide after Blue Owl halts redemptions at fund,” 20 February 2026

- Financial Times, “How Blue Owl’s battles sparked a chill for private credit,” 26 February 2025

- Financial Times, “How private equity’s big bet on stfware was derailed by AI,” 12 February 2026