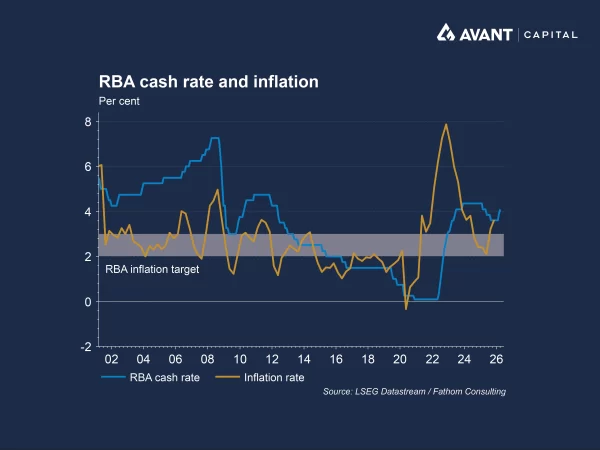

Why did the RBA raise rates again, and what is driving the inflation resurgence?

The Reserve Bank of Australia’s decision to raise the cash rate by 25 basis points to 4.10 per cent marks its second consecutive monthly increase in 2026, delivered through a tightly split 5–4 board vote1. The Board’s statement makes clear that inflation had already picked up materially in the second half of 2025, with the unemployment rate slightly lower than expected and capacity pressures proving stronger than previously assessed. Governor Michele Bullock emphasised that “inflation was already too high, reflecting the fact that demand is outstripping supply,” highlighting that domestic inflation pressures, not just geopolitical shocks, motivated the tightening cycle2.

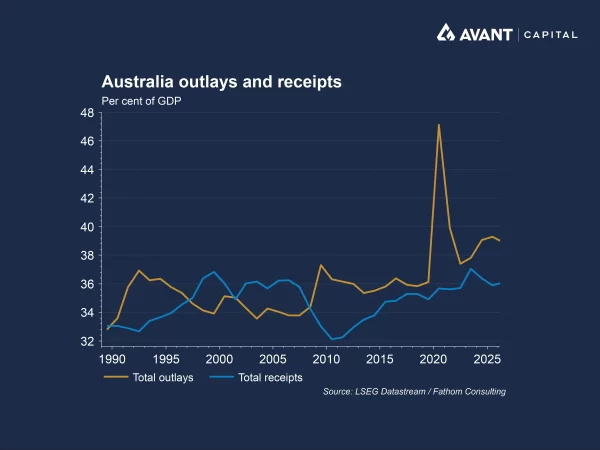

Government spending has played a key role over recent years. Prior to the Middle East conflict, inflation had re‑accelerated amid a combination of private‑sector demand recovering and the highest levels of government spending in nearly four decades outside the pandemic period, pushing the economy beyond its supply‑side limits. Treasury expects inflation to reach the “high 4s” this year, in part due to structural imbalances predating the oil shock3. Treasurer Jim Chalmers has acknowledged that “we had an inflation challenge before the dramatic escalation of hostilities in the Middle East,” even as he argues spending is not to blame.

How is the Iran conflict and oil shock influencing the RBA’s outlook?

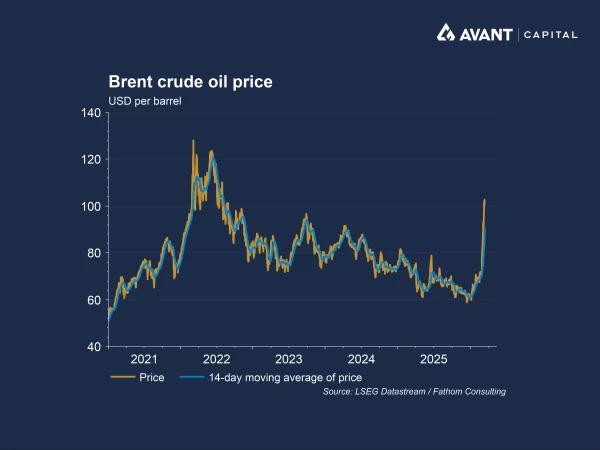

The RBA’s statement explicitly cites the Iran‑related conflict and resulting oil price spike as a key driver of upside inflation risk. Brent crude has surged above $US100 per barrel, sharply lifting petrol prices in Australia, with bowsers charging above $2 per litre. The Board warns that “the conflict in the Middle East has resulted in sharply higher fuel prices, which, if sustained, will add to inflation,” and further noted that higher energy costs may both lift near‑term inflation and weigh on global growth simultaneously, a dual‑risk environment the RBA cannot ignore.

Bullock stressed that while petrol prices will add to inflation, “they’re not the reason for today’s decision,” rather, the concern is that a fuel shock layered on top of existing inflation pressures could entrench inflation expectations if left unaddressed.

What is the RBA signalling about future decisions and economic risks?

The RBA remains cautious about the path ahead, acknowledging significant uncertainty surrounding domestic economic conditions, global developments, and how restrictive current policy settings truly are. While some board members preferred to wait until May for additional data before considering another rate hike, the majority ultimately judged that delaying action risked falling further behind the inflation challenge. Bullock said the RBA is “well placed to respond to developments” and will adjust policy as necessary to deliver price stability while attempting to avoid recession; however, she openly conceded that a downturn may become unavoidable if inflation proves stickier than anticipated.

The possibility of additional tightening remains live. Money markets price around a 50 per cent chance of another move in May, reflecting lingering uncertainty around the duration of the Iran conflict and its inflationary impact.

How are markets reacting, and what does this mean for investors?

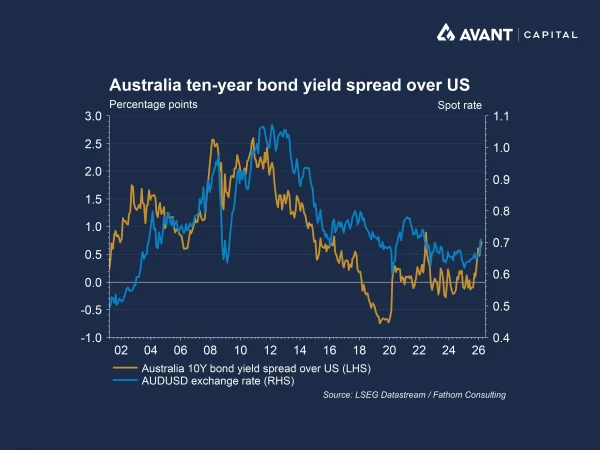

Bond markets have swung sharply, with Australian government bond yields climbing to multi‑year highs as traders adjust their expectations for further tightening. Longer‑dated bonds have been hit hardest because their interest rates are locked in for many years, making them less attractive when new bonds are issued at higher yields. As a result, their prices fall more when rates rise.

The Australian dollar appreciated materially in early 2026 as markets priced in a more aggressive RBA tightening cycle. A widening gap between Australian and US 10‑year government bond yields supported the currency, as higher relative yields made AUD‑denominated bonds more attractive to global investors, boosting demand for the AUD. More recently, however, this strength has begun to unwind as the conflict in Iran has escalated and investors have shifted toward safe‑haven US‑dollar‑denominated assets.

Equity markets present a mixed picture. Rate‑sensitive and economically cyclical sectors, such as consumer discretionary and housing‑related stocks, are likely to face pressure as higher borrowing costs weigh on household budgets and dampen spending. By contrast, consumer staples have shown relative resilience given their more stable demand profile, while financials such as banks and insurers can benefit from a higher‑rate environment.

Banks may see improved net interest margins, although this can be tempered by slower credit growth as households and businesses become more cautious. Insurers, meanwhile, can earn higher investment income on their “float,” the pool of premiums they collect upfront and invest before claims are paid, meaning rising rates lift the returns generated on these funds. Still, elevated valuations across the ASX 200 and a softening consumer outlook could limit broader market optimism.

The index has not fallen significantly despite rising rate expectations, and valuations remain above historical averages. This resilience may leave markets more exposed if sentiment shifts or economic conditions deteriorate.

References

- Reserve Bank of Australia, “Statement by the Monetary Policy Board: Monetary Policy Decision,” 17 March 2026

- The Australian Financial Review, “RBA lifts interest rates now, to avoid recession later,” 17 March 2026

- The Australian Financial Review, “Treasury tips inflation to hit the ‘high 4s,’” 12 March 2026