The escalation of the conflict in Iran has sent a clear and forceful signal through global bond markets. Far from acting as a traditional “flight to safety,” government bonds have sold off sharply, pushing yields higher across major economies. At the heart of this reaction is a renewed inflation shock driven by energy prices, combined with a rapid reassessment of how central banks may need to respond if inflation expectations become unanchored.

Why has the Iran conflict pushed government bond yields higher?

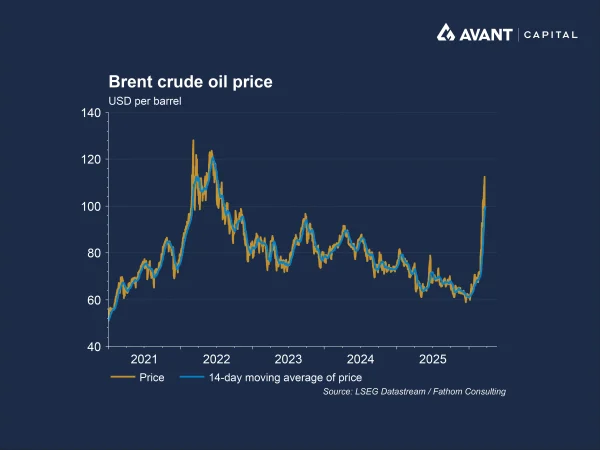

The most immediate transmission channel from the conflict to bond markets has been energy. Disruptions to oil and gas flows through the Strait of Hormuz, a critical chokepoint for roughly one-fifth of global energy shipments, have driven oil prices sharply higher. For bond investors, this matters because energy shocks feed directly into headline inflation and, more importantly, risk spilling over into broader price pressures.

Inflation erodes the real value of fixed coupon payments, making bonds less attractive unless yields rise to compensate. As a result, investors have demanded higher yields, particularly at the short end of yield curves where expectations for central bank policy are most acute. This dynamic has been visible across the US, UK, Europe and Australia.

How have expectations for central bank interest rates shifted?

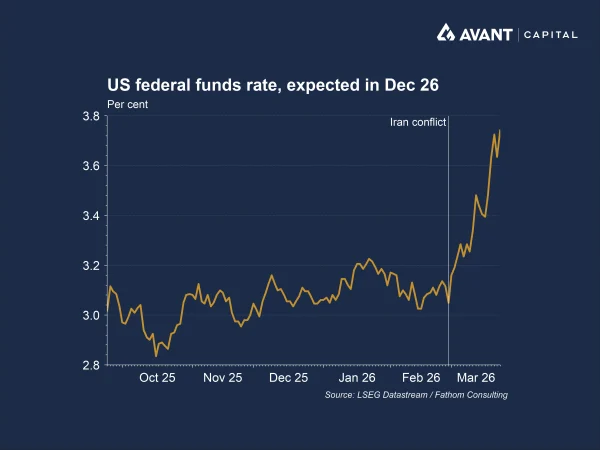

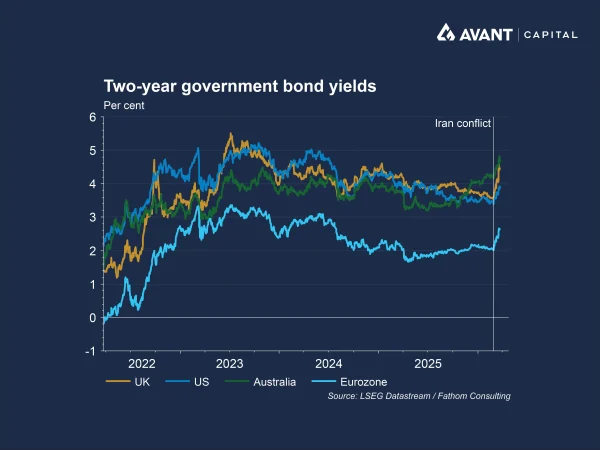

Perhaps the most striking feature of the bond market reaction has been the speed with which expectations have flipped from rate cuts to rate hikes. In the US, markets that were previously pricing two or three Federal Reserve rate cuts in 2026 have instead begun to price a meaningful chance of rate increases1. The two‑year US Treasury yield has risen by around half a percentage point since the war began, reflecting fears that the Fed may need to lean against inflation for longer.

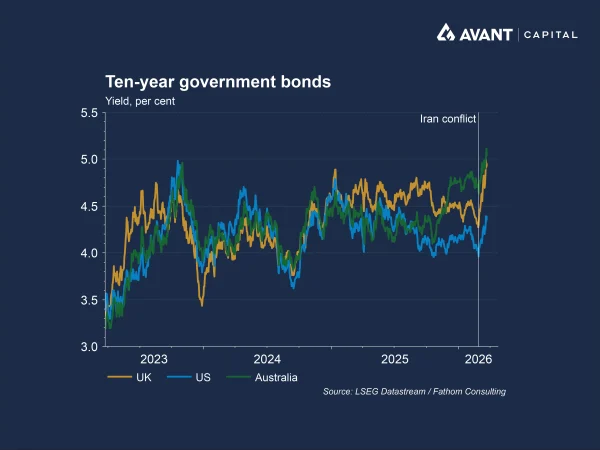

In the UK, the move has been even more dramatic. Ten‑year gilt yields have surged to around 5 per cent, their highest level since 2008, while two‑year yields, the most sensitive to Bank of England policy, have jumped sharply as traders price in as many as three or four rate rises this year2. Before the conflict, markets were expecting cuts. Similar repricing has occurred in Australia, where three and ten‑year government bond yields have climbed to multi-year highs as investors bet the Reserve Bank may need to tighten further.

Why has the UK gilt market been hit so hard?

While the energy shock is global, the UK bond market has been singled out for particularly severe moves. One reason is the UK’s heavy reliance on imported gas, which makes inflation more sensitive to energy prices than in the US or parts of Europe. UK one‑year inflation expectations have risen markedly since the conflict began, far outpacing comparable moves elsewhere.

Market structure has also amplified the move in gilts. The growing presence of hedge funds and other price‑sensitive investors has made the market more vulnerable to abrupt shifts in sentiment. Crowded trades that had been positioned for falling yields were rapidly unwound as oil prices surged and the Bank of England adopted a more hawkish tone. The result was a self‑reinforcing sell‑off that echoed the gilt turmoil seen during the 2022 “mini‑Budget” crisis.

Could inflation expectations become the bigger problem?

Central banks typically try to “look through” temporary energy shocks. However, the persistence and scale of this shock have raised concerns about second‑round effects, where higher fuel costs feed into wages, services inflation and long‑term expectations. Evidence of this risk can be seen in the rise in break‑even inflation rates, particularly in the UK, where ten‑year inflation compensation has increased by around 0.44 percentage points since late February3.

If long‑term inflation expectations drift higher, central banks may feel compelled to keep policy tighter for longer, even as growth slows. This fear has been a key driver of rising yields at the long end of yield curves, not just the short end.

What other forces could push bond yields higher over time?

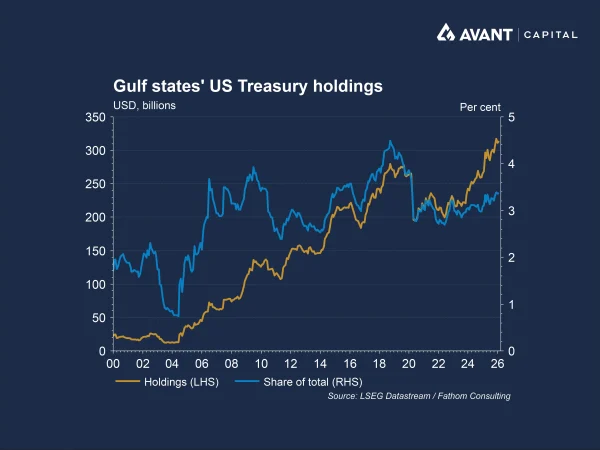

Beyond inflation and central bank policy, structural forces linked to the conflict could also push yields higher. Gulf states have become systemically important sources of global liquidity, running current account surpluses of more than $US800 billion over the past four years4. If geopolitical pressures lead them to redirect capital towards domestic infrastructure spending and security needs, global bond markets could lose an important source of demand, adding further upward pressure on yields.

Another factor is fiscal pressure. Governments are already running large deficits and face heavy refinancing needs. Higher yields increase debt‑servicing costs, which can create a feedback loop: rising interest expenses weaken public finances, prompting investors to demand even higher yields.

Is the bond market overreacting or underestimating future risks?

Some argue markets have moved too far, too fast, particularly at the short end of yield curves. With economic growth already slowing, central banks may ultimately opt to look through energy‑driven inflation as transitory and refocus on easing policy to limit the risk of a sharper downturn. Others contend that markets are only beginning to price the risk of a prolonged conflict, ongoing energy disruption and the possibility that inflation becomes more deeply entrenched. What is clear is that the conflict in Iran has pushed bond markets into a far more uncertain and fragile regime.

References

- Financial Times, “Iran war sends US borrowing costs soaring by most since 2024,” 24 March 2026

- Financial Times, “Gilt yields surge to highest level since 2008,” 23 March 2026

- Financial Times, “Chart of the Week: Global rates show deeper war fears,” 21 March 2026

- Financial Times, “Iran war is a risk to the flow of Gulf funds around the globe,” 23 March 2026