Why has gold declined despite escalating conflict in Iran?

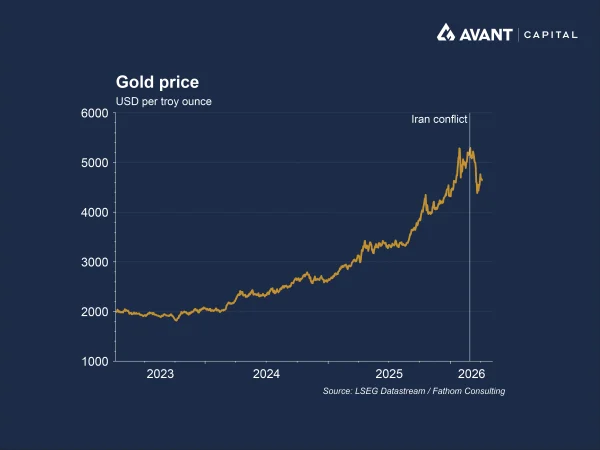

Gold’s sharp pullback in recent months has confounded many investors. Traditionally viewed as a safe-haven asset, gold would normally be expected to rally during periods of war and geopolitical instability. Yet since the outbreak of the Iran conflict in late February, the gold price has fallen sharply from its January peak, erasing most of its gains for the year. This decline has occurred even as tensions in the Middle East intensified, energy supply risks increased and broader financial markets experienced bouts of volatility.

The explanation lies less in geopolitics alone and more in market mechanics. Gold entered the conflict period from a position of extreme strength. Prices had surged to a record high above $US5,500 per ounce in January, driven by strong speculative inflows, heavy exchange-traded fund (ETF) demand and sustained central bank buying1. That left gold vulnerable to profit-taking once market stress emerged. As equities and bonds sold off sharply following the US-Israeli bombing of Iran, investors were forced to raise liquidity elsewhere, and gold, one of the most liquid and profitable positions, became a source of cash rather than a refuge.

How have liquidity pressures and margin calls weighed on prices?

A recurring theme across market commentary has been the role of margin calls and forced deleveraging. During periods of broad market stress, investors often sell assets that have performed well in order to meet collateral requirements or cover losses in riskier positions. Hedge funds and other leveraged investors liquidated bullion positions as the conflict in Iran triggered sharp losses across equity and bond markets. Gold was sold to meet margin calls and raise liquidity, reinforcing downward pressure on prices.

This dynamic is not unusual. Historical episodes such as the global financial crisis and the early stages of the pandemic also saw gold fall initially before later recovering. The scale of the recent sell-off, however, has been amplified by how crowded the gold trade had become prior to the conflict.

What role have interest rates and inflation expectations played?

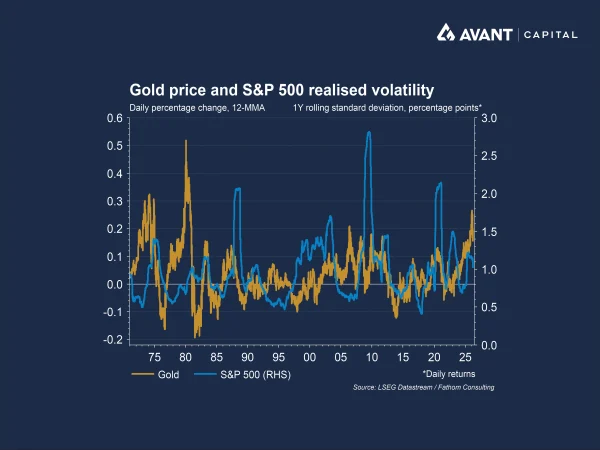

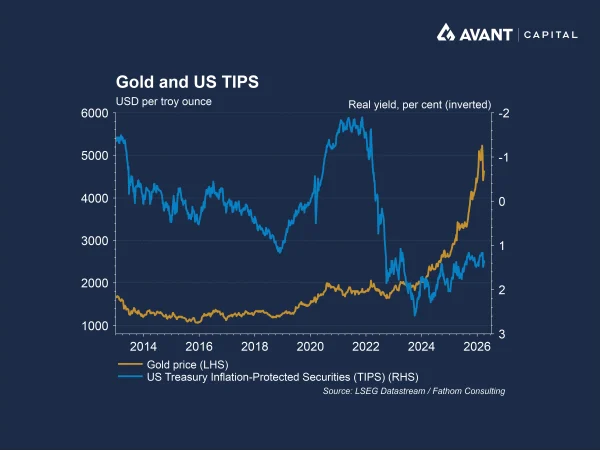

Another important driver has been the shift in interest rate expectations. Gold is highly sensitive to real yields because it offers no income. Before the war, markets had been pricing in multiple US interest rate cuts for 2026. The conflict-driven energy shock, however, has pushed inflation expectations higher and led central banks to signal that rates may need to stay “higher for longer.”

As those expectations adjusted, real yields rose and the opportunity cost of holding gold increased. This reassertion of the traditional inverse relationship between gold prices and interest rates has been a key factor behind the metal’s decline. Several analysts have noted that while this relationship weakened in recent years due to aggressive central bank gold buying, it has resurfaced during the Iran conflict as rate-cut hopes faded.

Why have central banks shifted from buyers to sellers?

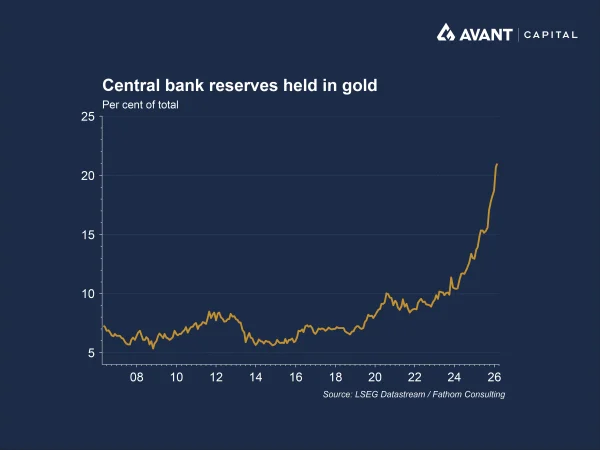

Central banks were a major pillar of support for gold during its multi‑year rally, but recent behaviour has become more mixed. While global central banks were net buyers of gold in 2025, purchases slowed materially, and some institutions have now turned into sellers2. Turkey has been the most prominent example, selling or swapping roughly $US20 billion worth of gold in March to support the lira and shore up foreign‑currency liquidity. In the Gulf, the economic fallout from the conflict, including infrastructure damage, higher security spending and a slowdown in travel and tourism, may similarly increase funding pressures, raising the likelihood that some states draw on gold reserves to support rebuilding efforts and cushion weaker growth.

These sales have challenged the assumption that central banks would act as a consistent backstop for prices. Although some countries, including China, have continued to buy opportunistically on weakness, the emergence of two-way central bank flows has added to near-term volatility and undermined confidence in gold’s defensive credentials.

Does gold still function as a portfolio diversifier?

The recent drawdown has reignited debate about gold’s role as a portfolio diversifier. Critics argue that gold has failed precisely when it was most needed, falling alongside equities and bonds rather than offsetting losses. The dominance of speculative and ETF-driven flows has also made prices more volatile, impacting gold’s reliability as a stabilising asset in the short term.

Supporters counter that this critique misunderstands gold’s function. Gold is not designed to provide immediate protection during every market shock, but rather to preserve purchasing power over longer horizons and across economic regimes. Historically, gold has tended to perform well during recessions, periods of sustained inflation and episodes of currency debasement, conditions that may still lie ahead if the Iran conflict prolongs energy disruptions and fiscal pressures.

What lessons does this episode offer investors?

The recent sell-off highlights that gold’s behaviour during crises is complex and path-dependent. In the short term, liquidity needs, positioning and interest rates can overwhelm safe-haven demand. Over longer periods, however, gold’s structural drivers, high global debt, geopolitical fragmentation and concerns about fiat currencies, remain intact.

References

- Financial Times, “Tumbling gold price puts ‘haven’ status in doubt,” 25 March 2026

- Financial Times, “Turkey’s gold sales deepen bullion slump,” 7 April 2026