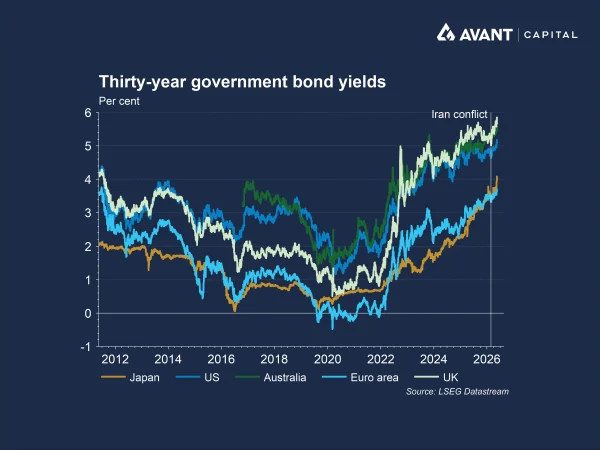

Why have government bond yields risen so sharply?

Government bond yields have risen sharply across most major economies in recent weeks as bond prices have come under sustained pressure. Yields and prices move in opposite directions because bonds pay a fixed stream of interest payments. When investors demand a higher return, due to rising inflation risks or greater economic uncertainty, existing bonds become less attractive, causing prices to fall until yields rise enough to entice new buyers.

What has stood out in the latest move is its global and synchronised nature. Long‑dated government borrowing costs in the United States, Japan, the UK and Australia have all risen to levels not seen for many years. This reflects a combination of renewed inflation concerns, geopolitical risks, heavy government borrowing and a material shift in expectations for central bank policy1.

How has the Iran conflict and energy shock affected bond markets?

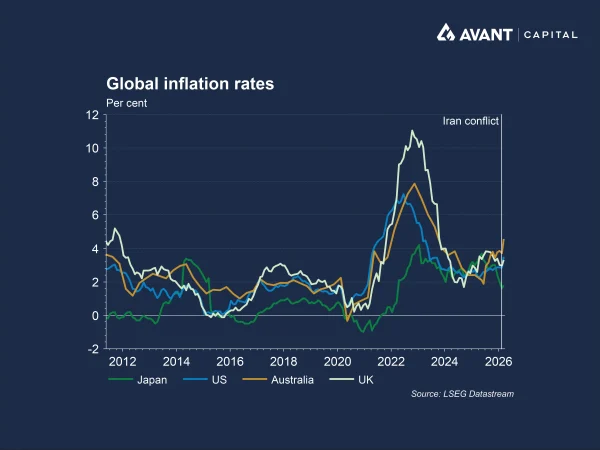

A key driver of the surge in government bond yields has been the ongoing conflict involving Iran and the continued disruption to global energy supplies. The closure of the Strait of Hormuz, a vital artery for global oil flows, has pushed energy prices sharply higher, feeding directly into fuel, transport and production costs across the global economy2.

Bond investors are highly sensitive to inflation, as rising prices erode the real value of fixed interest payments over time. As a result, energy‑led inflation fears have prompted investors to demand higher yields as compensation. Global oil inventories are being drawn down at a rapid pace, increasing the risk that inflation pressures persist rather than fade quickly. This has been enough to unsettle long‑dated bond markets in particular, where inflation risk is felt most acutely.

Why are central bank expectations shifting so dramatically?

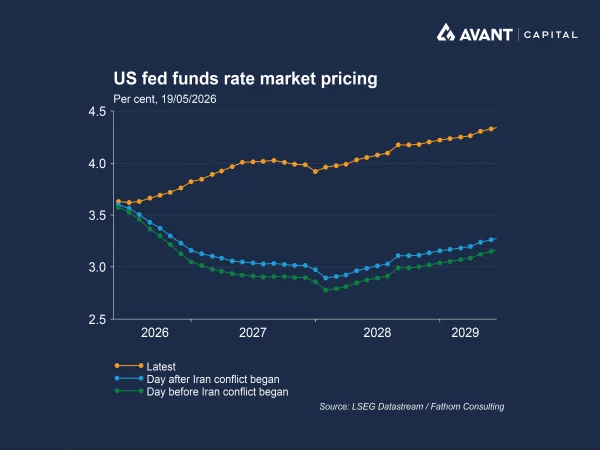

Before the escalation in the Middle East, markets were largely positioned for rate cuts in the US and other developed economies. That narrative has changed rapidly. Stronger‑than‑expected inflation data, combined with higher energy prices, has forced investors to reassess the likely path of monetary policy.

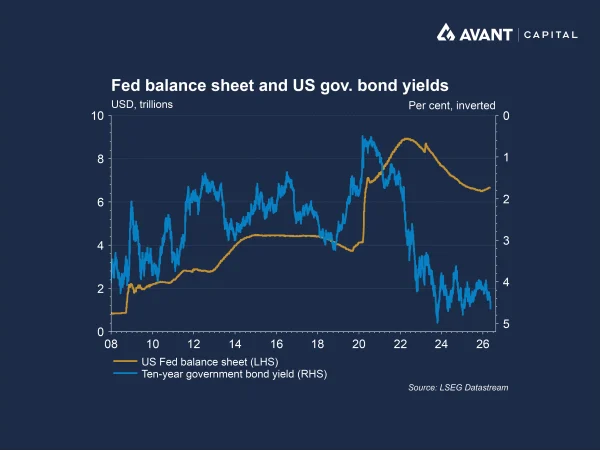

In the US, futures markets have shifted from pricing easing to assigning a meaningful probability to further rate increases. Adding to this shift is the prospect of a more hawkish policy stance under the new Federal Reserve chair, Kevin Warsh. Warsh has been a long‑standing advocate of shrinking the Fed’s balance sheet, which would involve allowing bonds held by the central bank to mature without reinvestment, or actively selling securities.

For bond markets, this matters because central banks have been major buyers of government debt over the past decade. If the Fed steps back from purchasing bonds, or becomes a net seller, a significant source of demand is removed. Private investors must absorb more government issuance, and that typically requires higher yields to clear the market. This dynamic has reinforced upward pressure on long‑dated government borrowing costs, with the US Treasury issuing 30‑year debt at yields above 5 per cent for the first time since 20073.

How are government debt levels and fiscal pressures contributing?

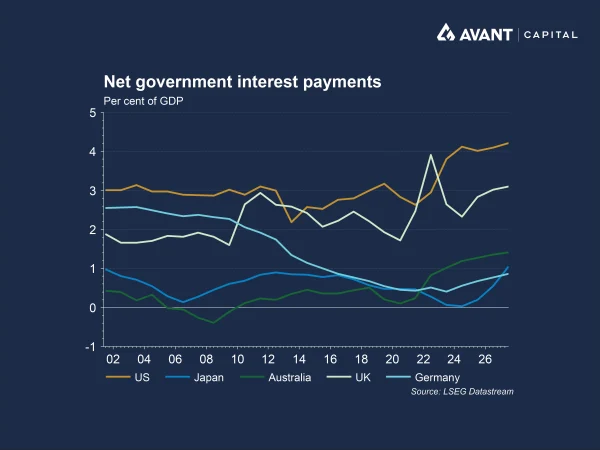

Rising yields are also being driven by concerns about government debt and fiscal sustainability. Many governments entered this period with already elevated debt levels following years of fiscal deficits. Higher yields mean governments must refinance maturing debt at significantly higher costs, increasing interest expenses and adding strain to public finances.

In Australia, recent budget announcements have unsettled bond investors, with projections showing gross debt continuing to rise and government spending remaining historically high as a share of GDP. More broadly, governments have increasingly relied on issuing short‑dated debt to limit interest costs. While this can reduce borrowing costs initially, it exposes governments to refinancing risk, as debt must be rolled over more frequently. When yields rise quickly, higher interest rates feed through to budgets faster, amplifying investor concerns.

What role is Japan playing in the global bond sell‑off?

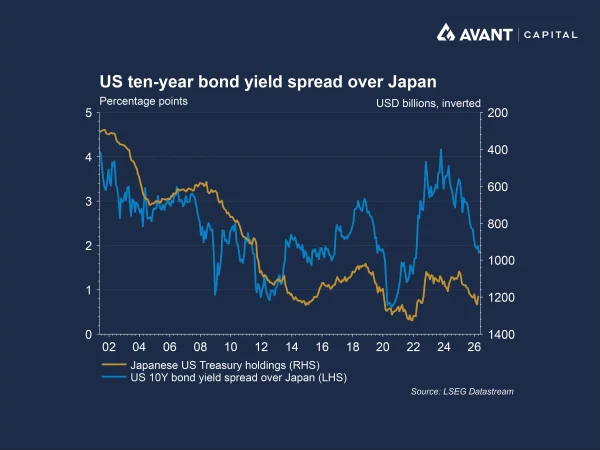

Japan has emerged as a critical factor in global bond markets. After decades of ultra‑low yields, Japanese government bond yields have surged as inflation has finally taken hold and the Bank of Japan has stepped away from its long‑running yield‑curve control policies4.

This shift has raised the possibility that Japanese investors, among the largest holders of foreign bonds, including US Treasuries, may begin repatriating capital back into domestic bonds. Reduced demand from Japanese investors for overseas government debt would place further upward pressure on yields elsewhere, reinforcing the global nature of the bond sell‑off.

Why do higher bond yields matter for equity markets?

Despite the turbulence in bond markets, global equity indices remain near record highs. However, these gains have been driven by a narrow group of mega‑cap technology and semiconductor companies, closely linked to the artificial intelligence investment theme.

Asset markets do not move in isolation. Rising bond yields increase the market’s risk‑free rate, the return available on low‑risk government bonds, which is used to discount future cash flows. This is particularly important for growth companies, such as technology firms, where a large share of valuation is based on earnings expected many years into the future. When discount rates rise, the present value of those future cash flows falls, placing pressure on valuations.

At the same time, higher government bond yields can encourage capital reallocation away from equities. When investors can earn more attractive returns from relatively low‑risk assets, the additional return demanded for holding equities increases.

How are credit markets responding to higher bond yields?

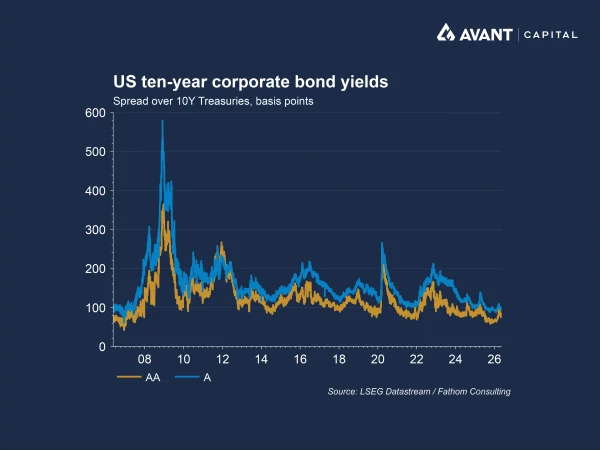

Credit markets have so far remained relatively resilient, with credit spreads still tight by historical standards. This suggests investors are currently comfortable with corporate balance sheets and default risks, particularly among higher‑quality borrowers. However, this calm may be tested if the economic effects of higher energy prices begin to flow through more forcefully. A sustained rise in fuel costs linked to the Iran conflict risks weighing on consumer spending and corporate margins, which could weaken earnings and increase credit risk. In that environment, credit spreads could widen, especially if growth slows more sharply than expected.

Higher government bond yields also change the relative appeal of credit. As yields on low‑risk government bonds rise, investors may demand greater compensation for holding corporate debt, or reallocate capital away from credit altogether. This dynamic has the potential to tighten financial conditions further, reinforcing pressure across both equity and credit markets.

How does the AI‑led rally increase market vulnerability?

The concentration of market gains around AI and semiconductor stocks has amplified these risks. Valuations across parts of the technology sector already embed high expectations for earnings growth and strong returns on substantial capital investment in data centres and computing infrastructure.

This leaves markets more vulnerable to disappointment. If bond yields continue to rise, or if AI earnings growth fails to meet expectations, equity markets could become more volatile. With a relatively small group of AI‑linked stocks driving a large share of market gains, any shift in sentiment toward the theme can have an outsized impact on the broader market.

Taken together, the sharp rise in government bond yields is reshaping the global investment landscape, lifting borrowing costs, tightening financial conditions and increasing the risk that elevated valuations across asset markets are tested as risk‑free returns become more attractive.

References

- The Wall Street Journal, “The global bond rout is accelerating. Here’s what to know,” 19 May 2026

- Financial Times, “Global bonds tumble on fears of inflation shock from Iran war,” 16 May 2026

- Financial Times, “US sells 30-year bonds at 5% yield for first time since 2007,” 14 May 2026

- Financial Times, “Record high Japanese yields trigger bets on repatriation,” 17 May 2026