Across big tech, finance and corporate America more broadly, layoffs are clearly mounting. Yet when set against still‑resilient headline employment data, the picture is far more nuanced. The emerging story is less about a sudden AI‑driven employment cliff and more about a slow squeeze on white‑collar hiring, especially at the entry level, taking place against a backdrop of heavy AI capital spending, cautious CEOs and a labour market that is cooling unevenly.

Are AI‑linked layoffs accelerating in the US?

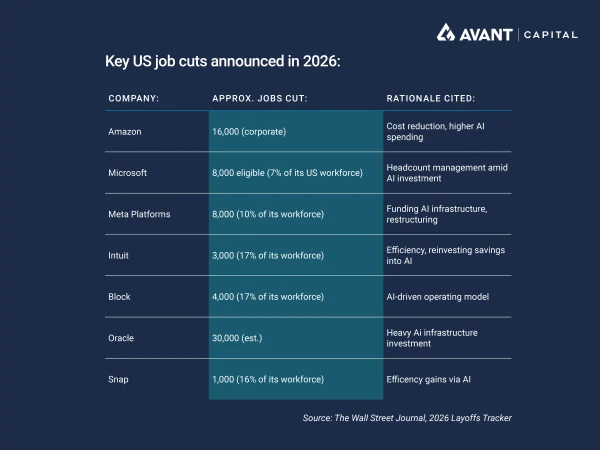

Recent announcements have been striking. Microsoft is offering voluntary redundancy to roughly 7% of its US workforce1, Amazon has outlined another 16,000 corporate job cuts2, Meta is cutting around 8,000 roles3, and Intuit is slashing 17% of staff while explicitly redirecting savings into AI investment4. Across the tech sector, outplacement firm Challenger, Gray & Christmas data shows announced job cuts running 33% higher in the first four months of this year versus last year5.

What is notable is not just the scale, but the framing. Executives increasingly reference AI as a reason for becoming “leaner,” “flatter” or more “efficient.” In many cases, AI spending is soaring at the same time headcount is falling. Microsoft alone plans to spend about $US140 billion on AI infrastructure this year, while Meta and Amazon are also committing tens of billions to data centres and chips.

Yet this does not automatically mean AI is already replacing workers at scale. In several cases, management teams have acknowledged that the cuts are about simplifying layers, removing middle management, or correcting post‑pandemic over‑hiring rather than deploying fully autonomous AI systems

Are CEOs cutting jobs because markets expect it?

Another explanation sits squarely with investor psychology. Equity markets have rewarded companies that demonstrate “discipline” on costs, particularly while pouring capital into AI. Revenue per employee has become a closely watched metric on earnings calls, and layoffs mechanically improve it.

In that sense, AI can function as a socially acceptable justification. Saying “AI lets us do more with fewer people” sounds forward‑looking and strategic. Saying “we are padding margins, hedging macro uncertainty, and responding to shareholder pressure” is less compelling.

What do the jobs numbers actually show?

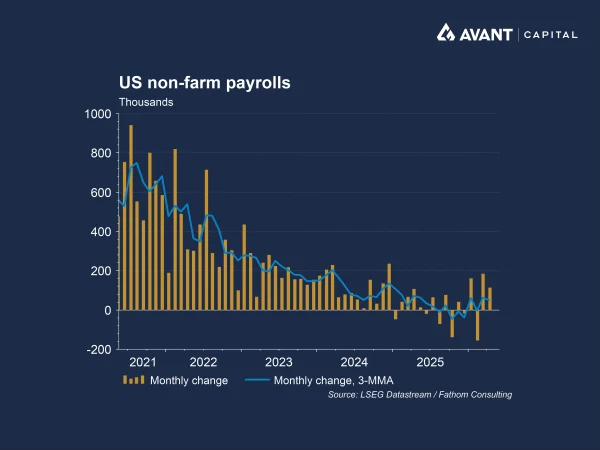

Despite the headlines, US labour market data remain surprisingly resilient. The economy added 115,000 jobs in April, beating expectations, and the unemployment rate held at 4.3%7. Weekly initial jobless claims remain low by historical standards, suggesting there has not yet been a broad‑based firing cycle. Where weakness is emerging is on the hiring side, not the firing side. Job openings are down, hiring rates are subdued, and underemployment has risen.

This divergence helps explain why layoffs feel omnipresent while aggregate data still look “fine.” For people entering the workforce or trying to move jobs, conditions are tightening materially.

Why are young and entry‑level workers feeling it first?

Youth unemployment is flashing amber. In the US, unemployment among college graduates aged 22–27 has risen close to levels last seen during the global financial crisis. Hiring for graduate and junior roles has slowed sharply, particularly in tech, consulting, finance and corporate functions.

AI plays an indirect role here. Entry‑level tasks are often routine, process‑driven and text‑based, exactly where generative AI is most immediately useful. Even if AI is not “replacing” workers outright, it is reducing the marginal need to hire new ones. Firms are asking existing staff to do more, assisted by AI tools, rather than expanding headcount.

Does this point to a K‑shaped economy?

The broader implication is a deepening K‑shaped economy. In simple terms, a K‑shaped recovery or expansion is one where different groups experience sharply different outcomes. Those exposed to asset markets, capital returns and ownership of AI infrastructure are thriving, while those reliant on wages, especially younger or less established workers, lag behind.

AI threatens to turbo‑charge this dynamic. Productivity gains accrue disproportionately to capital owners, software platforms and the AI supply chain, while wage growth remains modest. Asset markets, particularly US equities, continue to outperform labour income growth by a wide margin. Layoffs and weaker entry‑level hiring risk widening the disconnect between those “inside” the asset‑rich economy and those outside it.

Could AI still be more about augmentation than replacement?

There is a counter‑argument worth taking seriously. Many companies stress that AI is augmenting existing workers rather than replacing them. Tools that automate drafting, coding assistance, customer support triage or data analysis can lift productivity without shrinking teams dramatically. In this scenario, fewer new hires are needed, but mass unemployment does not materialise.

History supports this view. Past technological shifts, from computers to the internet, ultimately raised productivity and incomes, but only after long adjustment periods. Goldman Sachs research suggests AI may displace around 6–7% of US jobs over a decade, not overnight, with younger workers often adapting more successfully than older cohorts8.

How does Australia compare?

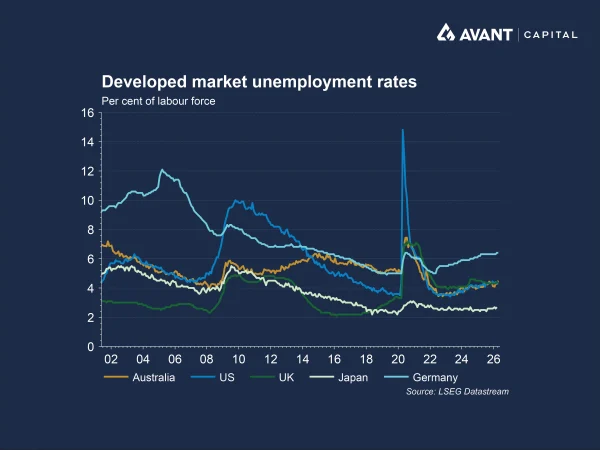

Australia may experience this transition differently. Strong industrial relations protections, higher redundancy costs and more rigid labour markets make rapid headcount reductions harder to execute. That could mean fewer layoffs in the short term. But it also risks slower realisation of productivity gains from AI, potentially leaving Australian firms less competitive and dampening returns on AI investment.

Recent Australian data already shows youth unemployment rising to 11.1%, the highest since October 2021, and suggesting hiring caution is filtering through even without mass layoffs9. As in the US, the stress point appears to be at the margins of the labour market rather than its core.

What should investors take away?

AI is not yet driving a sharp rise in unemployment, but by restraining hiring and lifting efficiency it increases the risk that labour‑market softness eventually weighs on consumer spending.

For markets, the focus has been on the upside: productivity gains allow companies to protect margins and sustain earnings even as demand cools. The result is a growing divergence between strong corporate performance and a labour market that is tightening at the edges, with important implications for both growth and asset prices.

References

- Financial Times, “Microsoft to offer 7% of US staff voluntary redundancy for the first time,” 24 April 2026

- Financial Times, “Amazon to axe another 16,000 corporate jobs,” 28 January 2026

- The Wall Street Journal, “Meta begins laying off thousands of employees as it transforms around AI,” 20 May 2026

- Reuters, “Intuit trims annual TurboTax revenue forecast, to cut 17% of workforce,” 21 May 2026

- The Wall Street Journal, “How to make sense of this strange job market,” 8 May 2026

- The Wall Street Journal, “2026 Layoffs tracker: Walmart, Meta and Morgan Stanley among firms cutting jobs,” 12 May 2026

- The Wall Street Journal, “US adds 115,000 jobs in April with solid hiring across sectors,” 8 May 2026

- Financial Times, “Earnings expectations are too high,” 8 April 2026

- The Australian Financial Review, “Youth job losses push unemployment rate to 4.5%,” 21 May 2026