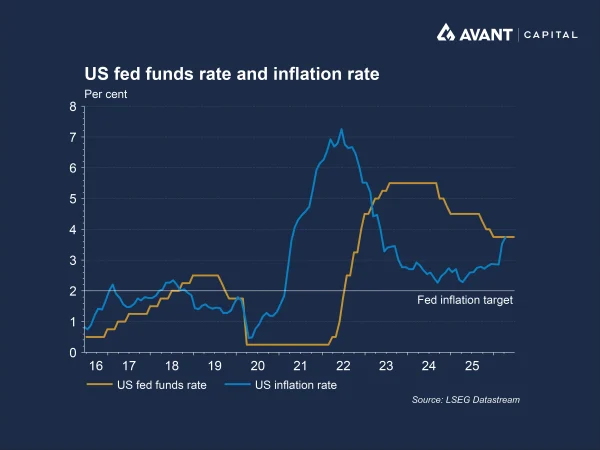

Kevin Warsh’s first meeting as chair of the Federal Reserve marked a clear inflection point for US monetary policy, even without an outright change in interest rates. The Federal Open Market Committee (FOMC) voted unanimously to keep the federal funds rate on hold in a range of 3.5-3.75%, extending the current pause in policy as the Fed reassesses its next move1.

However, the decision itself was overshadowed by a meaningful shift in tone and expectations. The Fed abandoned its previous bias toward easing policy, signalling that the next move is more likely to be a rate increase rather than a cut. This pivot reflects growing concern among policymakers that inflation pressures, exacerbated by the recent Iran conflict and energy shock, remain too persistent to justify looser monetary conditions.

Crucially, the shift was broad-based. There were no dissenting votes, suggesting Warsh successfully aligned a committee that had been more divided in recent meetings. Even so, the decision to hold rates can be seen as tactical rather than dovish, allowing policymakers time to assess evolving inflation dynamics while preparing markets for a tougher stance ahead.

How did Warsh communicate his priorities and outlook?

Warsh used his first press conference to deliver a simple but forceful message: inflation control is the Federal Reserve’s overriding objective. His repeated assertion that the Fed “will deliver price stability” underscored a strong commitment to restoring credibility after years of above-target inflation2.

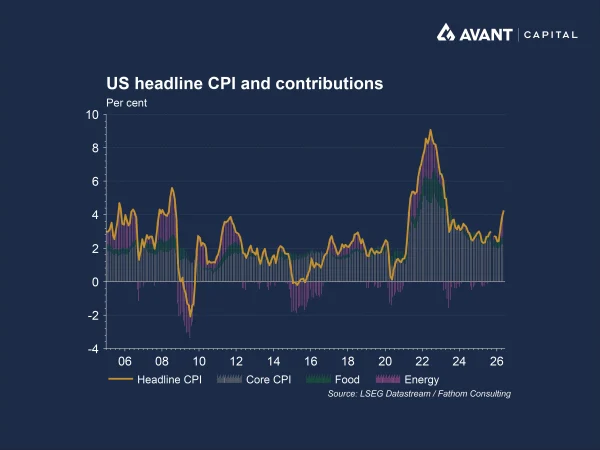

This focus is motivated by persistent inflationary pressures. The Fed’s preferred gauge of personal consumption expenditures inflation is running at around 3.8%, almost double its 2% target, with projections suggesting only a modest decline to 3.6% by year-end. That would mark the sixth consecutive year of missing its inflation goal, raising concerns about credibility and inflation expectations becoming unanchored.

Warsh also struck a careful balance between flexibility and firmness. While he declined to explicitly signal rate increases, he stated that they could not be ruled out, even as soon as the next meeting, reinforcing the perception of a hawkish bias. Underlying this message is a clear priority: the Fed is prepared to tolerate tighter financial conditions to ensure inflation is brought under control.

What did the Fed’s projections and market reaction reveal?

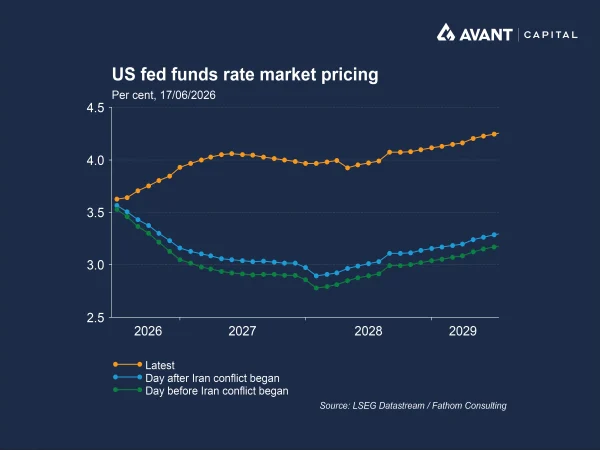

Perhaps the most significant development from the meeting was the sharp shift in policymakers’ projections. Nine of 19 officials now expect at least one rate hike by the end of the year, compared with none just three months earlier3.

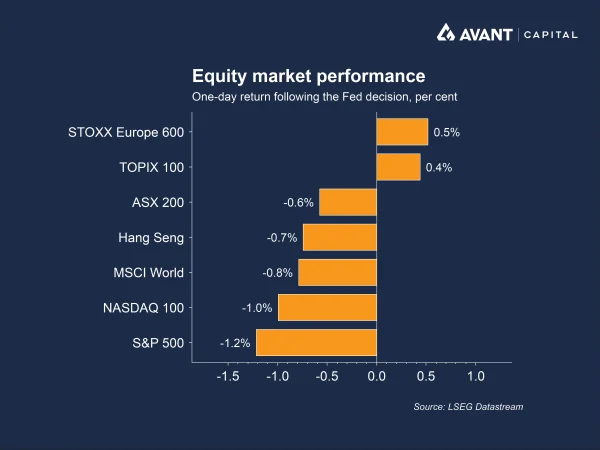

This abrupt change caught markets off guard. Equity markets fell, with the S&P 500 declining around 1.2%, while Treasury yields rose sharply, the two-year yield climbing to roughly 4.2%, the highest in 16 months, and the 10-year approaching 4.5%4. Investors quickly recalibrated expectations, shifting from anticipated rate cuts earlier in the year to pricing in a strong likelihood of hikes in the coming months.

The bond market reaction was particularly telling. Short-term yields surged as traders reassessed the Fed’s trajectory, reflecting the central bank’s renewed resolve to tighten if necessary.

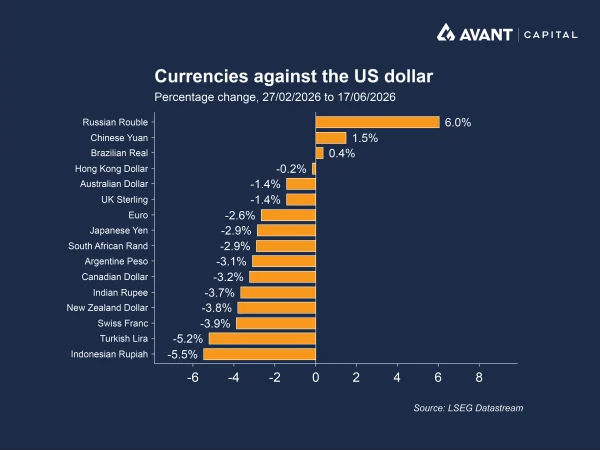

Meanwhile, the US dollar strengthened, further signalling tighter financial conditions ahead.

How is Warsh reshaping the Fed’s communication strategy?

One of the most striking features of Warsh’s first meeting was how little the Fed said. The policy statement was unusually brief, around 132 words, and removed much of the detailed guidance that had characterised previous communications5.

Warsh has made clear that he is sceptical of forward guidance, and the meeting marked a deliberate move away from signalling the likely path of interest rates. He declined to provide his own “dot plot” projections, and the statement omitted cues that previously hinted at easing.

This approach represents a significant shift in how the Fed interacts with markets. Rather than guiding expectations with precise forecasts, Warsh appears to prefer strategic ambiguity, leaving markets to interpret the data and the Fed’s broader objectives.

While this may reduce the risk of policy errors driven by rigid commitments, it also introduces greater volatility. Markets responded sharply to the lack of guidance, underscoring how reliant investors had become on the Fed’s signalling under previous leadership.

What broader reforms could reshape the Fed under Warsh?

Beyond the immediate policy stance, Warsh’s first meeting hinted at a broader agenda to reform the Federal Reserve’s operations. He announced the creation of five task forces to review core aspects of the institution, including communications, data usage, inflation frameworks and the balance sheet.

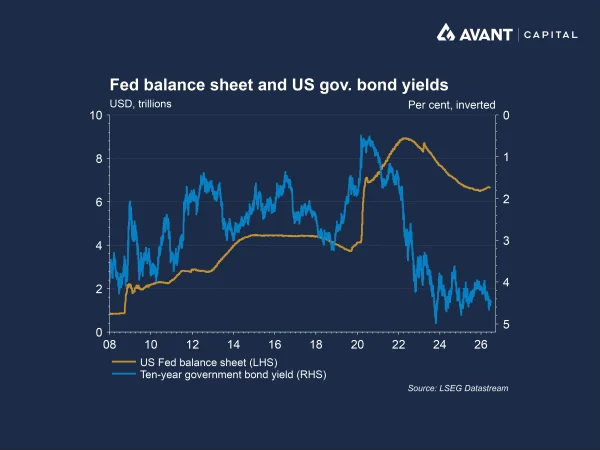

These initiatives suggest a willingness to reconsider long-established practices. In particular, Warsh has flagged interest in shrinking the Fed’s balance sheet over time, a move that could have important implications for financial markets. As a major buyer of US Treasuries, the Fed’s reduced presence could place upward pressure on long-term yields, tightening financial conditions even without changes to the policy rate. At the same time, his emphasis on improving data quality reflects concerns that traditional economic indicators may lag real-time developments in an increasingly fast-paced economy.

Taken together, these reforms point to a central bank that may become leaner, less predictable and more reliant on market discipline, marking a departure from the highly communicative and interventionist approach of recent years.

What does this mean for the outlook of US monetary policy?

Warsh’s first meeting signals that the Federal Reserve is entering a new phase defined by higher-for-longer rates and a renewed focus on inflation control. With inflation still elevated and economic activity holding up, policymakers appear increasingly willing to tighten further if necessary. At the same time, the Fed’s evolving communication strategy suggests markets will need to operate with less explicit guidance, amplifying uncertainty around the timing and magnitude of future moves.

Ultimately, the early message from Warsh is clear: the Fed is prepared to prioritise credibility over comfort. While the immediate decision was to hold steady, the broader direction of travel points toward a more hawkish and less predictable policy regime, one that could reshape expectations across global markets in the months ahead.

References

- The Wall Street Journal, “Fed holds rates steady, but more officials see higher rates as next move,” 17 June 2026

- Financial Times, “Federal Reserve officials tilt towards rate rise as Kevin Warsh era begins,” 18 June 2026

- The Wall Street Journal, “Warsh’s commitment to inflation fight sparks market slide,” 17 June 2026

- Financial Times, “Federal Reserve officials tilt towards rate rise as Kevin Warsh era begins,” 18 June 2026

- The Wall Street Journal, “Five takeaways from Kevin Warsh’s first meeting as Fed Chairman,” 17 June 2026