What has traditionally made emerging markets a diversifier?

Emerging markets (EMs) have long been seen as a cornerstone of global diversification. Historically, they offered exposure to different growth cycles, commodity dynamics, currencies and policy regimes that were largely independent from developed markets (DMs). Investors gained access to sectors underrepresented in developed markets, particularly energy, resources and financials, alongside distinct macroeconomic drivers such as US dollar cycles, commodity price shifts and domestic policy regimes.

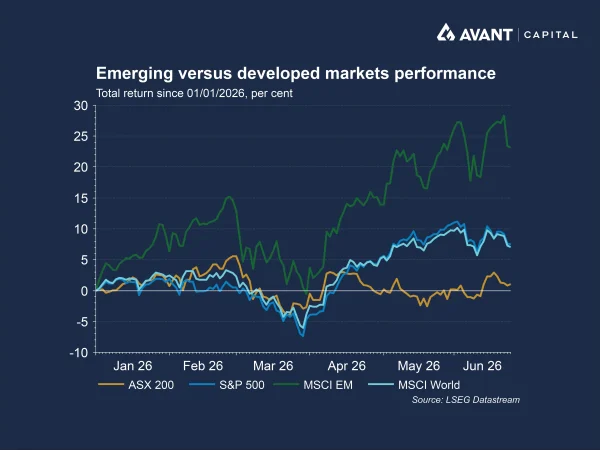

However, this traditional framework is increasingly being challenged. Over the past year, emerging markets have outperformed developed markets, while becoming more closely tied to global growth narratives, particularly one dominant theme: artificial intelligence.

How has the AI theme reshaped emerging market indices?

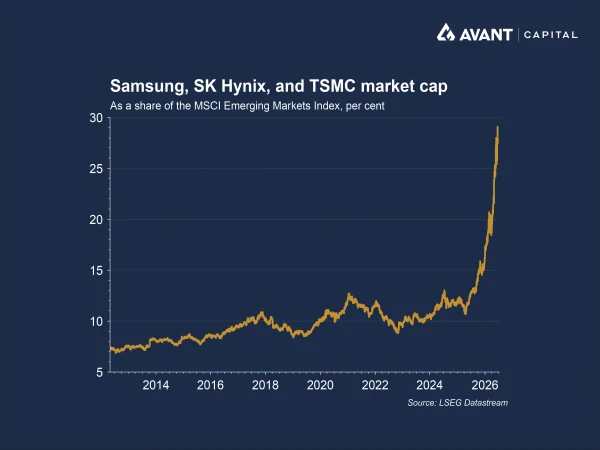

The most striking shift in emerging markets has been the rapid concentration of index weightings in a handful of semiconductor companies central to the global AI buildout. Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics and SK Hynix now account for an outsized share of the MSCI Emerging Markets index, transforming it from a broad, diversified basket into a more tech-heavy exposure.

This concentration is significant. Just a small number of chipmakers now drive a substantial share of index performance, with roughly half of this year’s gains attributable to TSMC, Samsung and SK Hynix, whose shares have surged sharply amid booming demand for AI infrastructure1.

As a result, emerging markets are increasingly being driven by the same forces shaping developed markets, namely the capital expenditure cycle of hyperscalers and global demand for advanced semiconductors. Rather than reflecting a range of independent economic drivers, EM performance has become more closely tied to a single global theme.

This shift has important implications for diversification. Historically, EMs offered exposure to different growth cycles, currencies and commodity trends. Today, their growing correlation with Wall Street, particularly the technology sector, means that market movements in US AI stocks can quickly transmit through to emerging market benchmarks. Recent volatility in global chipmakers, driven by changing expectations around AI spending and interest rates, has highlighted how quickly sentiment can spill across regions.

The result is an asset class increasingly shaped by one dominant narrative, reducing the breadth of underlying return drivers that investors have traditionally relied on for diversification.

Where is divergence appearing within emerging markets?

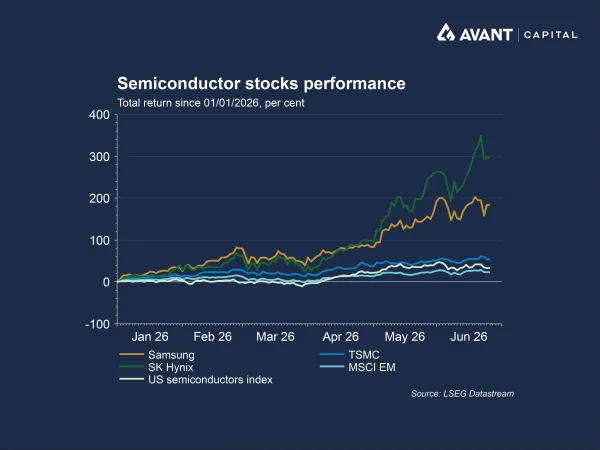

Despite the overarching AI trend, performance within EMs has diverged significantly across regions. South Korea and Taiwan have been the clear beneficiaries, driven by their leadership in semiconductor production and their integration into global AI supply chains.

By contrast, other major EMs have lagged. India, for example, has underperformed due to its lack of “pure-play” AI exposure. Foreign investors have pulled approximately $US26.4 billion from Indian equities this year, as the country lacks large-scale chipmakers or AI infrastructure companies2.

China presents a different story. While parts of its AI supply chain have rallied, large technology companies such as Alibaba and Tencent have underperformed, with investors favouring hardware providers and smaller “pure AI” firms instead3.

This divergence highlights that, while AI is a dominant global theme, its benefits are unevenly distributed, creating winners and losers within emerging markets.

What geopolitical risks should investors consider?

The increasing concentration of EM indices in semiconductor leaders also introduces geopolitical considerations, particularly in Taiwan. As a critical hub for global chip production, Taiwan sits at the centre of strategic tensions, adding a layer of geopolitical risk to index exposure.

These dynamics suggest that EM investors are now implicitly exposed to geopolitical developments tied to global technology supply chains, rather than solely to domestic economic conditions.

Are traditional EM drivers still relevant today?

While AI dominates the narrative, traditional macro drivers of emerging markets have not disappeared, they have simply become less visible in driving short-term returns.

The US dollar remains a key factor. Historically, EM equities perform well when the dollar weakens, as it reduces the burden of US dollar‑denominated debt across emerging economies and lowers financing costs. Recently, however, a resurgence in the dollar, driven by expectations of higher US interest rates, has pressured EM currencies and reversed earlier gains.

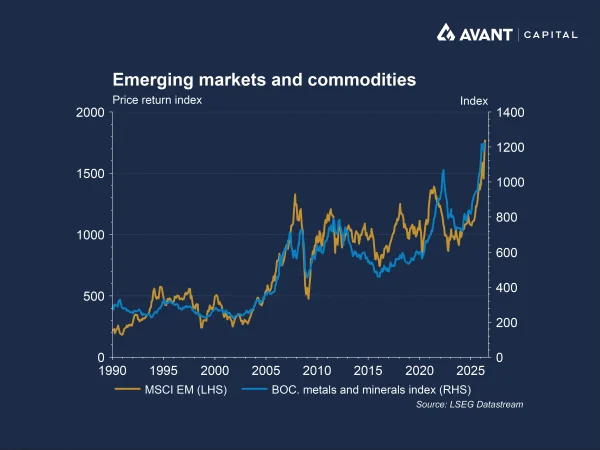

Commodity prices are another important influence. Higher oil prices stemming from the Iran conflict have added pressure across emerging markets, many of which are net energy importers, driving inflation higher and complicating the outlook for central banks. This limits their ability to ease policy and support growth. At the same time, emerging markets remain major commodity producers, such as Brazil in iron ore and agriculture, and Chile in copper, meaning price moves can have mixed effects across the asset class.

Encouragingly, EM macroeconomic frameworks have strengthened in recent years. Improved central bank credibility, built through more proactive and disciplined rate hikes during past inflation cycles, has enhanced resilience even as higher energy costs continue to pose challenges. Government debt dynamics have also improved relative to developed markets, with EM sovereign debt levels generally rising more slowly and, in many cases, remaining lower than their developed market peers, marking a contrast to previous cycles when EM balance sheets were more vulnerable.

These factors still materially affect returns, but their impact can be overshadowed when a dominant thematic driver, such as AI, takes centre stage.

What does this mean for emerging markets going forward?

Emerging markets are not losing relevance, but they are evolving. The rise of AI has brought them closer to developed markets in both structure and performance drivers. In many ways, this reflects a broader convergence: EMs are increasingly integrated into global supply chains and capital markets, particularly in high‑growth sectors like technology. However, this convergence comes at a cost. The diversification benefit that once defined EM investing has been diluted by concentration risk and thematic overlap with developed markets. Despite the AI‑driven rally, emerging markets still trade at a meaningful discount to developed markets, reflecting structural perceptions of higher risk and volatility, even as underlying fundamentals have improved and the composition of indices has become more technology‑oriented.

Ultimately, emerging markets are no longer a single, broad-based diversification tool. Instead, they represent a more complex and fragmented opportunity set, one that requires a deeper understanding of both global themes and local drivers.

References

- Financial Times, “Tech boom brings emerging markets and their rich cousins closer together,” 8 May 2026

- Financial Times, “Indian stocks lose out to Asian rivals in global hunt for AI winners,” 4 June 2026

- Financial Times, “China’s big tech groups miss out on AI stock market frenzy,” 13 May 2026