What exactly has changed in bank capital regulation, and why now?

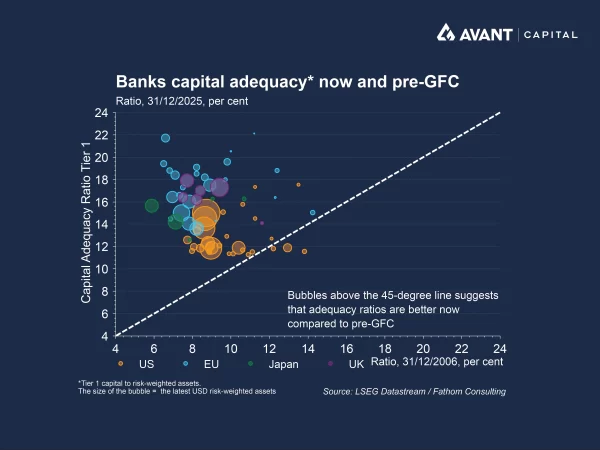

US regulators have announced a significant recalibration of bank capital rules, marking one of the most consequential shifts in post‑global financial crisis regulation in nearly two decades. Under the revised proposals, the largest US banks would face an average reduction of around 4.8 per cent in required capital once the combined effects of Basel III implementation changes, stress‑test adjustments and tweaks to the global systemically important bank (GSIB) surcharge are taken into account1. Midsized banks would see capital requirements fall by about 5.2 per cent, while smaller lenders could benefit from reductions closer to 7.8 per cent. These changes represent a sharp reversal from the earlier “Basel Endgame” proposals floated in 2023, which would have lifted capital requirements for major banks by as much as 19 per cent.

To understand why this matters, it is important to clarify what looser bank capital rules mean in practice. Bank capital refers to the equity and retained earnings that banks are required to hold as a buffer against losses. When regulators reduce capital requirements, banks are able to support a larger volume of lending and other assets for a given amount of equity, reflecting greater regulatory confidence in balance‑sheet strength. Put simply, each dollar of bank capital can back more loans. While this does not compel banks to lend, it does provide greater balance‑sheet capacity to do so, potentially increasing the availability of credit to households and businesses where demand exists.

Why have regulators opted to ease capital buffers rather than tighten them?

Officials argue the revisions better align capital requirements with actual risk, while simplifying a framework that has grown increasingly complex over time. Federal Reserve leadership has framed the move as a recalibration rather than a deregulation, emphasising that capital levels would remain “robust” even after the reductions.

The shift also reflects political and economic realities. Banks have spent years lobbying against what they saw as excessive constraints that limited lending and pushed activity into less regulated corners of the financial system, particularly private credit. Regulators now appear more concerned about credit migrating outside the banking system than about marginally lower capital ratios inside it.

How much capital could be freed up, and where might it go?

In absolute terms, the implications are large. The eight US global systemically important banks hold close to $US1 trillion in capital, and Federal Reserve estimates suggest the new rules could lower required capital by roughly $US20 billion, with some policymakers arguing the true figure could be closer to $US60 billion once all changes are incorporated2. Analysts have also pointed out that uncertainty around final rules has already led banks to accumulate excess buffers; Morgan Stanley estimates around $US175 billion of surplus capital is sitting on balance sheets. As clarity emerges, that capital could be released through a mix of increased lending, greater capital markets activity and higher shareholder distributions.

What does this mean for credit growth and the broader economy?

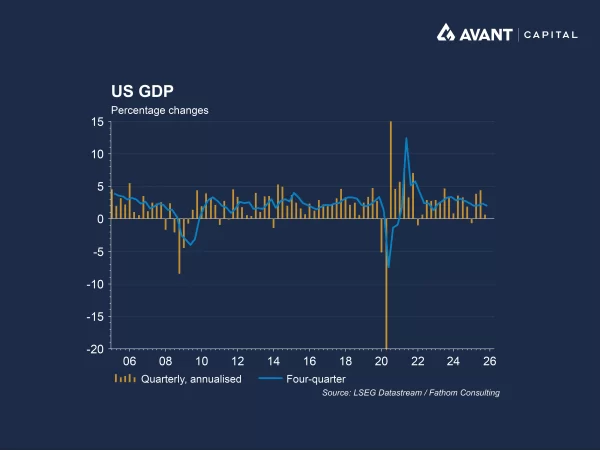

In theory, lower capital requirements should support an expansion in bank lending, particularly at a time when economic momentum is slowing. The US economy has already shown signs of cooling, with fourth‑quarter growth slowing sharply and job losses beginning to mount. Against this backdrop, regulators appear keen to ensure banks are not a brake on activity. However, history suggests the relationship between capital rules and lending is not mechanical. Demand for credit, borrower quality and economic confidence will matter at least as much as regulatory capacity. There is also a risk that banks prioritise buybacks and dividends over lending, particularly if loan demand remains weak.

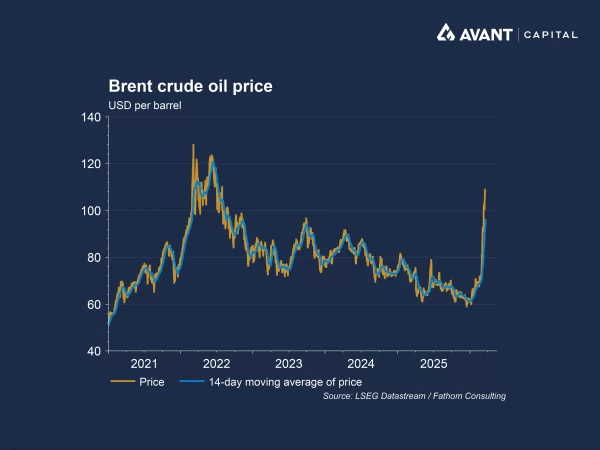

Does the timing matter given the growing risk of an oil‑driven slowdown?

The regulatory pivot comes as global markets grapple with a renewed oil shock following conflict in the Middle East. Oil prices have surged towards $US100 a barrel, pushing up inflation expectations and complicating the task of central banks. Federal Reserve officials have acknowledged that higher energy prices could lift headline inflation in the near term, even as growth slows and labour markets weaken.

This combination of softer activity and renewed price pressures raises the risk of a stagflation‑like environment. In that context, easing bank capital rules may operate as a countercyclical buffer, ensuring the financial system can continue to supply credit even if monetary policy remains tight.

Could there be longer‑term risks to financial stability?

Critics argue the changes come at an inopportune moment. Private credit risks are rising, geopolitical uncertainty is elevated and memories of the 2023 regional banking stress are still fresh. Some policymakers fear that a weaker version of Basel III in the US could trigger a global “race to the bottom,” pressuring other jurisdictions to loosen standards in the name of competitiveness3. While regulators insist safeguards remain strong, the true test will only come in the next downturn. Lower capital buffers increase sensitivity to shocks, even if they support growth in the short run.

Overall, the easing of bank capital rules represents a calculated attempt to support credit and economic resilience amid rising macroeconomic risks, but its success will depend on whether greater balance sheet flexibility translates into productive lending rather than simply higher returns to shareholders.

References

- Financial Times, “US regulators slash Wall Street capital rules to boost bank lending,” 19 March 2026

- Reuters News, “Wall Street bank capital to fall 4.8% under new rules, in win for industry,” 20 March 2026

- The Wall Street Journal, “Big Banks score win under new plan to loosen capital rules,” 19 March 2026