How did the conflict in Iran turn a regional war into a global oil shock?

The conflict between Iran, the United States and Israel has escalated into the most severe disruption to the global oil supply chain in decades. Iran’s effective closure of the Strait of Hormuz, a waterway through which around a fifth of the world’s oil normally flows, has choked off exports from much of the Persian Gulf and sent shockwaves through energy markets. According to Opec data, oil production across the cartel plunged by a record 27% in March as producers struggled to export crude and were forced to temporarily halt production when storage facilities filled up1. Production fell by 7.9 million barrels a day in a single month, eclipsing even the sharpest declines seen during the Covid-19 pandemic. The result has been a sudden, structural break in the flow of physical oil rather than a temporary price spike driven by sentiment.

Why has the Strait of Hormuz become the central fault line in the oil supply chain?

The Strait of Hormuz is the single most critical chokepoint in global energy trade, and its closure has created immediate physical shortages. Shipping through the strait has effectively stalled since late February. The International Energy Agency estimates that around 13 million barrels a day of oil production has been shut off by the conflict2. While emergency releases of strategic reserves totalling 400 million barrels have been announced, much of this oil cannot fully replace the lost Gulf supply because logistics, shipping routes and refinery configurations are not easily substituted. The disruption has been compounded by heightened security risks, making large areas of the Gulf effectively uninsurable for commercial tankers.

The same chokepoint is also central to global gas and fertiliser supply chains. The Middle East accounts for a large share of internationally traded nitrogen fertilisers, while natural gas, the key input for ammonia and urea, has surged in price and become scarcer as the conflict has disrupted energy flows. As fertiliser exports through the Gulf stall and gas shortages force plants to cut output across Asia and the Middle East, the effects extend beyond fuel markets into food production, manufacturing costs and broader supply chains, amplifying the economic impact of the conflict.

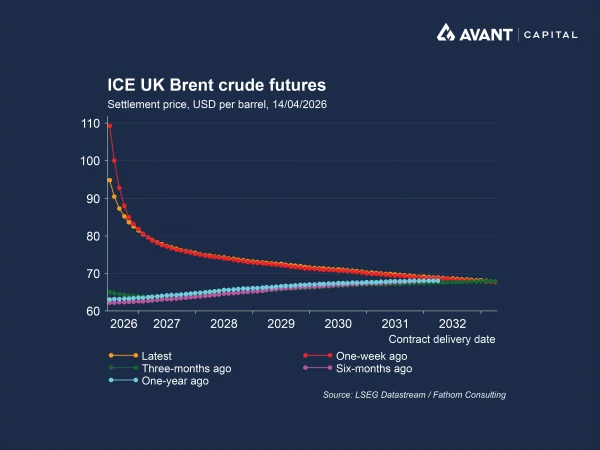

How has the war distorted oil prices and exposed cracks between futures and physical markets?

Oil prices have surged, but headline benchmarks have understated the severity of the shock. While Brent futures have hovered around $US100 a barrel, prices for physical crude have surged far higher. Dated Brent, which reflects actual cargoes for delivery, has traded well above $US130 a barrel, with some shipments delivered to Asia at $US150–170 a barrel once shipping costs are included3. This unprecedented gap reflects extreme scarcity in physical markets rather than speculative excess. Refiners have been forced to pay almost any price to secure barrels, squeezing margins and reducing output of fuels such as diesel and jet fuel. The result is a global supply chain under strain not just from cost inflation, but from an inability to access sufficient volumes at any price.

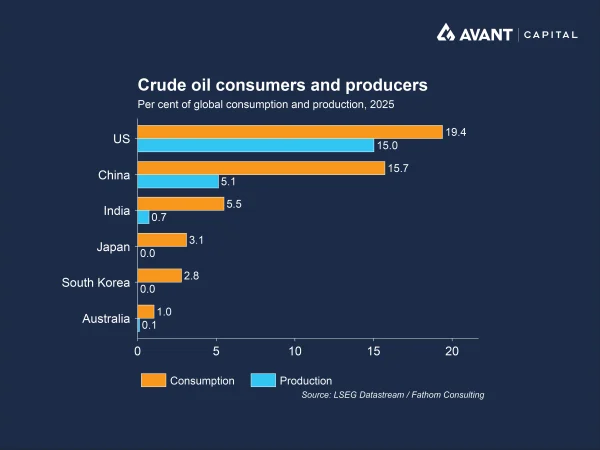

Why has Asia borne the brunt of the oil supply disruption?

Asia is the region most exposed to the closure of the Strait of Hormuz, as around 90% of the oil flows through the Strait head there. As pre-war cargoes reach their final destinations, refiners across Asia have been scrambling to secure replacement supplies from the US, Europe, Africa and Latin America. Arrivals of crude into Asia from within the strait have collapsed to about 4 million barrels a day in early April, compared with a normal level of more than 13 million barrels a day4. Several Asian economies have already felt the social impact, with countries such as the Philippines declaring energy emergencies after local fuel prices doubled.

How has Australia been affected?

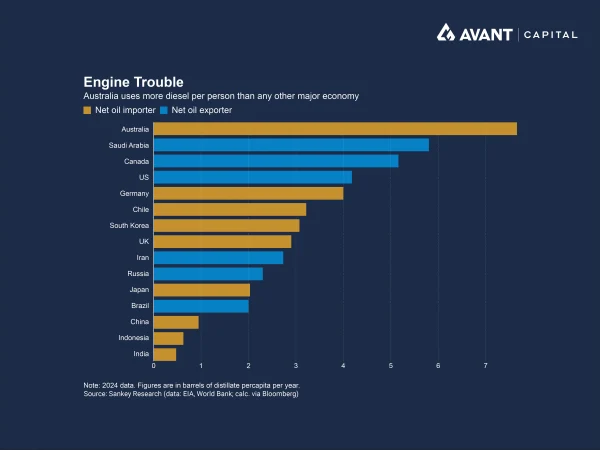

Australia’s exposure has been acute despite importing relatively little fuel directly from the Middle East. Petrol imports account for around 66% of demand, while diesel imports cover about 89% of domestic demand, and jet fuel imports account for roughly 80%5. Australia is due to receive its last pre-war cargo from the Middle East in mid-April, prompting the release of fuel reserves, tax cuts and the rollout of a national fuel security plan. Even so, analysts warn that structural shortages are likely if the conflict drags on.

The impact extends well beyond petrol prices. Higher diesel costs affect agriculture, mining and freight, while rising jet fuel prices weigh on aviation and tourism. Australia also faces an additional exposure through fertiliser markets, where global shortages and sharply higher prices, driven by gas disruptions and reduced output in key producing regions, are adding cost pressures for farmers.

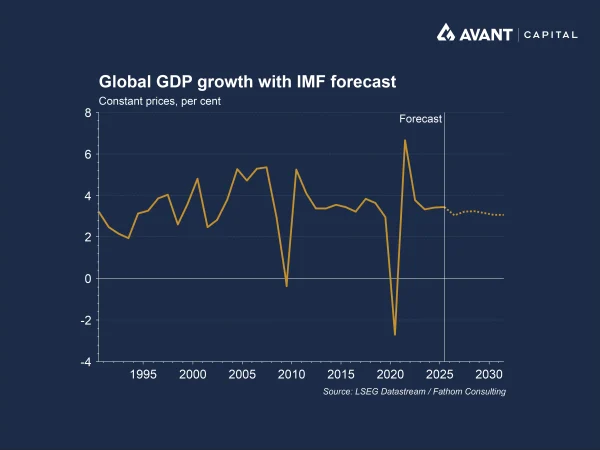

What does the oil shock mean for global growth and inflation?

The oil supply disruption has collided with an already fragile global economy. In its latest World Economic Outlook, the International Monetary Fund (IMF) said global growth was expected to be around 3.1% under its base forecast, assuming the conflict eases and energy prices fall back. However, the fund has warned that if oil prices remain around $US100 a barrel, global growth could slow to just 2.5% this year, the weakest pace since the pandemic. Under a more severe scenario, with oil prices rising to $US110–125 a barrel, global growth could fall to 2%, a level historically associated with recession, while inflation surges to around 5.8%6. Higher energy costs would then feed into food prices, transport costs and industrial production, raising the risk of stagflation across both advanced and emerging economies.

Even if a ceasefire holds, many analysts argue there will be no quick return to normal in the oil market. Damage to infrastructure, elevated geopolitical risk and continued disruption around the Strait of Hormuz could keep millions of barrels a day off the market. For energy‑importing regions such as Asia and Australia, the conflict has exposed the vulnerability of fuel supply chains. For the global economy, it has materially worsened the outlook, with the IMF warning that prolonged high oil prices could weigh on growth and delay the path back to lower inflation.

References

- Financial Times, “Opec production falls more than a quarter as Iran war hits oil exports,” 14 April 2026

- Financial Times, “Global oil demand plummets by most since pandemic, says IEA,” 14 April 2026

- Financial Times, “The US is at risk of an oil shock too,” 15 April 2026

- Financial Times, “Oil supply crunch intensifies as last Hormuz tankers reach refineries,” 14 April 2026

- Australian Financial Review, “Why Australia’s petrol problem is far from over (in four charts and a map),” 10 April 2026

- Financial Times, “Iran war could slow global growth to weakest since pandemic, IMF warns,” 14 April 2026