After several subdued years, the US initial public offering (IPO) market is poised for a dramatic revival. SpaceX, OpenAI and Anthropic are all preparing listings that could together command a combined market capitalisation of around $US4 trillion, or about 6% of the US public equity market, placing them among the most valuable companies ever to enter public markets1.

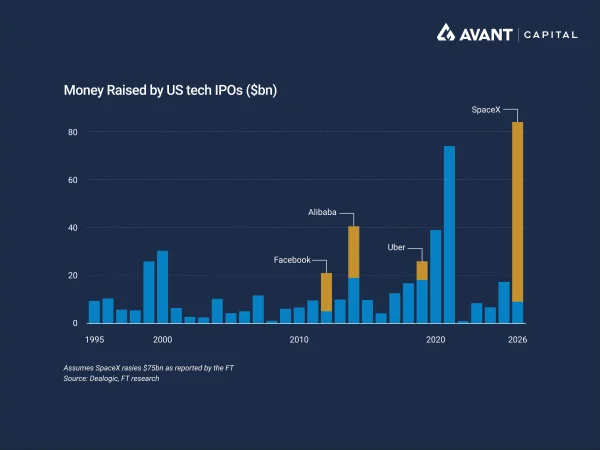

SpaceX alone is seeking to raise up to $US75 billion, a sum that would comfortably eclipse the $US29.4 billion raised by Saudi Aramco in 2019, the largest IPO to date2. Taken together, these deals would dwarf historical flotations and mark the first time public investors can directly access the leading developers of large language models (LLMs), rather than gaining exposure indirectly through semiconductor manufacturers or hyperscale cloud providers.

For Wall Street, this is not simply about deal volume. It is a test of whether public markets can absorb an unprecedented surge in equity supply at a time when valuations are already elevated and market leadership is unusually narrow.

What is driving investor enthusiasm for these listings?

The bullish narrative rests squarely on the AI trade. US equity markets have continued to reach record highs despite higher inflation and global bond yields stemming from the Iran energy disruption. Strong US earnings growth and accelerating AI adoption have helped sustain risk appetite, with AI investment increasingly becoming a structural driver of GDP growth.

Crucially, these IPOs offer something new: direct ownership of the AI labs themselves. Until now, public investors have largely been forced to express AI optimism through “picks and shovels” such as chips, servers and data centres. The prospect of owning the companies building frontier models has generated intense demand, with investors already rushing into funds and structured products designed to gain early exposure ahead of the listings.

How does public listing expose AI leaders to market pricing risk?

The listings of OpenAI and Anthropic mark a decisive shift in how these companies are valued. Once public, valuations that were previously set infrequently through private funding rounds will be exposed to continuous public‑market price discovery, leaving them far more sensitive to changes in sentiment. At current levels, those valuations are high, and could be re‑priced sharply if expectations around growth, execution or profitability are challenged.

For investors, this provides broader and more transparent access to AI’s upside, but also introduces greater downside risk. Public markets tend to show far less tolerance for missed milestones, rising losses or slower adoption. With a significant share of recent equity returns driven by AI optimism, any meaningful reassessment of these flagship valuations would not be confined to the stocks themselves, but could have broader implications for market sentiment and performance.

Why is fast index inclusion a critical risk factor?

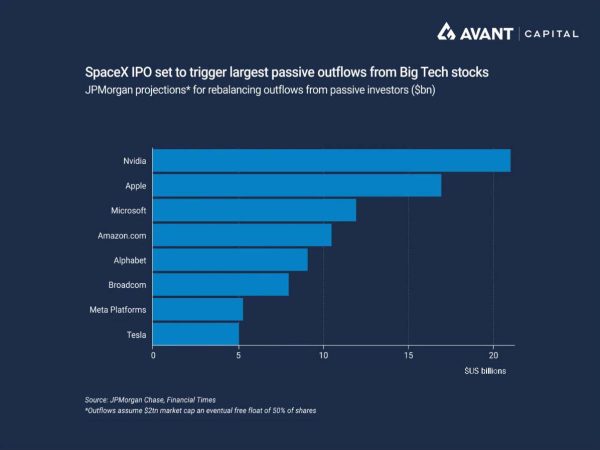

One of the most underappreciated dynamics is how quickly these stocks are likely to enter major equity market indices. New “fast‑entry” rules introduced by Nasdaq and other index providers mean SpaceX, OpenAI and Anthropic could be added to benchmarks such as the NASDAQ 100 within days or weeks of listing3.

This creates a mechanical chain reaction. Passive funds tracking indices will be forced buyers, regardless of valuation. To fund those purchases, they must sell other constituents, including members of the Magnificent 7.

JPMorgan estimates that if SpaceX were ultimately valued at around $US2 trillion and roughly half of its shares were made available to public investors over time, index rebalancing could force close to $US95 billion of selling from existing large‑cap technology stocks.

The effect is not merely rotational. It risks amplifying volatility, pushing index investors into newly listed stocks at inflated prices, while simultaneously pressuring incumbent market leaders.

Are valuations starting to echo the dotcom era?

Valuations are unavoidably part of the debate. SpaceX is targeting a valuation of around $US1.75 trillion, equivalent to more than 91 times trailing revenue. By comparison, Nvidia, the most expensive of the Magnificent 7 stocks on a revenue basis, trades at roughly 21 times revenue while generating substantial profits. OpenAI and Anthropic are also expected to list at or above the $US1 trillion mark4, despite heavy cash burn and loss‑making business models5.

Critics draw parallels with the late‑1990s dotcom boom, when a surge of late‑cycle IPOs coincided with market peaks. History shows that major equity issuance often precedes periods of weaker index performance as supply overwhelms marginal demand. Supporters counter that this time is different. Unlike many dotcom‑era listings, today’s AI leaders have explosive revenue growth, real enterprise adoption and strategic importance across the economy. The comparison, they argue, conflates speculative businesses with companies that sit at the core of a transformational technological shift.

How does equity supply and lock‑up risk complicate the outlook?

Initial floats are only the first wave. Lock‑up expiries over the following six to twelve months could release hundreds of billions of dollars of additional shares into the market. Lock‑ups are restrictions that prevent early investors and company insiders from selling their shares for a set period after an IPO, designed to avoid an immediate flood of stock hitting the market. Goldman Sachs estimates that expiring lock‑ups in 2026 could add close to $US500 billion in potential equity supply, a scale comparable to late‑cycle periods in previous market peaks6.

Markets may ultimately absorb this additional supply, but the process is unlikely to be frictionless. When large volumes of stock come to market, particularly at a time of elevated valuations, prices often need to adjust to clear that supply. The risk is not simply short‑term volatility, but that new issuance and post‑lock‑up selling compete for capital with existing equities, diluting demand across the broader market.

This matters because recent equity returns have been heavily driven by AI optimism, with investors willing to pay high multiples on the expectation of sustained growth and future profitability. In that environment, there is little margin for disappointment. If high‑profile IPOs underperform, or if insider selling accelerates once lock‑ups expire, valuations may need to reset lower, not just for the newly listed stocks, but potentially across the wider AI complex that has underpinned market performance.

What happens if the AI IPOs disappoint?

The broader risk is a feedback loop into market sentiment. Much of the US equity rally has been driven by AI optimism, even as bond markets price in persistent inflation, higher yields and tighter financial conditions. A weak reception for marquee AI IPOs would risk puncturing that narrative, prompting a reassessment of valuations across the technology sector and beyond.

That does not imply an imminent collapse. But it does suggest these IPOs are more than isolated corporate events. They represent a live test of whether AI enthusiasm can continue to support elevated equity valuations in the face of rising macroeconomic and geopolitical uncertainty.

References

- Financial Times, “Why IPO mania could signal top of the market,” 24 May 2026

- Financial Times, “SpaceX, OpenAI and Anthropic IPOs set to test limits of AI boom,” 23 May 2026

- Financial Times, “’Fast entry’ SpaceX, OpenAI and Anthropic IPOs to ignite Wall Street trading frenzy,” 22 May 2026

- Financial Times, “Anthropic files for blockbuster initial public offering,” 2 June 2026

- Financial Times, “OpenAI readies IPO filing to list as soon as September,” 21 May 2026

- Financial Times, “IPO boom, market doom?” 2 June 2026