Why has ASIC put private credit valuations under scrutiny?

Australia’s private credit market has grown rapidly over the past decade, becoming a roughly $224 billion sector as investors chased yield in a low-rate world1. But that growth has brought heightened scrutiny, culminating in a decisive intervention from the Australian Securities and Investments Commission (ASIC) ahead of the June 30 financial year end2.

Following an eight-week review of dozens of funds, ASIC warned that some loan valuations are “lagging economic reality” and may not fully reflect deteriorating borrower conditions. The regulator has since put the industry on notice: end-of-financial-year valuations must be “current, accurate and grounded in realistic assumptions”, or risk misleading investors and undermining outcomes.

This push comes at a pivotal moment. Private credit, particularly in Australia, is heavily concentrated in property lending, with exposures tied to development projects and underlying asset values. ASIC is concerned that opacity, inconsistent valuation methodologies, and lagged recognition of stress could mask rising risks, especially as the economic cycle turns.

What does Judo Bank reveal about emerging credit stress?

The timing of ASIC’s intervention coincided with a sharp shock from Judo Bank, which has become a critical case study for the sector. In late June, the SME-focused lender revealed three previously unidentified loans had deteriorated rapidly, forcing it to raise provisions by $20 million3.

The market reaction was immediate and severe: Judo’s share price fell around 40%, wiping roughly $400 million from its valuation. The fact that three unrelated loans across different industries soured simultaneously raised deeper questions. Was this an isolated issue, or an early signal of broader economic weakness?

Management emphasised that the deterioration was both rapid and largely unanticipated, with a small number of exposures worsening sharply over a short period. Yet analysts and investors were less convinced. The episode raised concerns about visibility across loan books and whether similar issues may soon emerge elsewhere, particularly as small business conditions soften.

Indeed, demand for SME credit has already dropped 7% year-on-year according to Equifax, while rising interest rates, inflation, and weaker consumer confidence are placing pressure on business borrowers. In this context, Judo may not be an outlier but rather an early indicator of stress building in credit markets.

How are federal budget changes and rate hikes compounding risks?

The macro environment has shifted sharply against both banks and private credit. Australia’s federal budget introduced sweeping changes to property investment incentives, including the effective removal of negative gearing benefits for new purchases of existing properties and tighter capital gains tax settings. The immediate impact has been a collapse in investor demand. Westpac reported a 20% drop in investor loan applications within weeks of the budget changes4.

Overlaying these structural shifts are higher interest rates. The Reserve Bank has delivered multiple rate increases, raising borrowing costs and putting pressure on both households and businesses. This combination, policy tightening and monetary tightening, is feeding directly into weaker credit growth, which analysts suggest could roughly halve in coming years.

For private credit, this matters profoundly. Many borrowers are now refinancing at higher rates, while the pool of new demand is shrinking. For lenders concentrated in property-backed loans, declining investor activity and tighter credit conditions create both refinancing risk and reduced deal flow, while also limiting liquidity and narrowing exit pathways as transactions slow and asset turnover declines.

What is happening in the property market and why does it matter for credit?

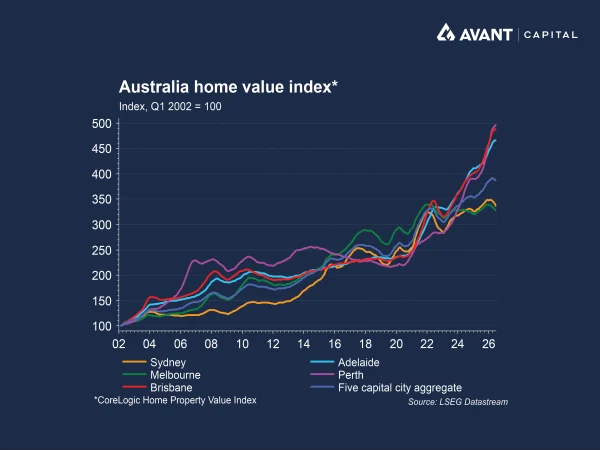

Property sits at the heart of the Australian private credit ecosystem, and recent trends have turned increasingly negative. House prices in Sydney and Melbourne are now falling, with declines accelerating in recent months. Prices in Sydney dropped 1.2% in June alone, while Melbourne fell 1%, contributing to a broader national downturn5. Transaction activity is also weakening, with auction clearance rates dropping to pandemic-era lows, nearly hitting 40% in June.

For private lenders, this environment introduces multiple and reinforcing risks. Lower property prices reduce the value of the underlying collateral, eroding the buffer that protects lenders if a borrower defaults. At the same time, weaker sales volumes mean projects take longer to sell, delaying cash inflows and pushing out repayment timelines. This increases the risk that loans need to be extended or restructured rather than repaid on time.

Developers are also facing rising construction costs, slower pre-sales and tighter financing conditions, making it harder to complete projects and refinance existing debt. While broader economic conditions have remained relatively stable to date, there is a growing risk they could deteriorate quickly as federal budget changes take effect and the cumulative impact of higher interest rates continues to flow through the economy. In a weaker market, lenders may be forced to support struggling borrowers for longer, accept lower recoveries, or ultimately realise losses if projects fail.

In short, the property cycle is no longer a tailwind, it is becoming a source of stress.

What risks does ASIC see for investors and the broader system?

Beyond valuations, ASIC’s concerns extend to investor outcomes and broader system risks. The regulator has warned that if loan valuations lag deteriorating conditions, investors may be given an overly optimistic view of performance, increasing the risk of misinformed decisions and unexpectedly weak returns when losses emerge.

ASIC has also highlighted structural issues across the sector, including inconsistent disclosure, unclear definitions of defaults and limited stress testing, which make it harder for investors to properly assess underlying risk. This is particularly relevant as credit conditions weaken and risks can remain hidden in private markets until they surface more abruptly.

There are also concerns about mis-selling, particularly as retail investors have been drawn into private credit funds on the basis of stable income and low volatility. In reality, these funds are exposed to illiquid loans and cyclical sectors such as property, where losses can emerge with a lag rather than in real time.

Liquidity is another key issue. Many funds invest in long-dated, illiquid loans but offer more regular redemption terms, creating a mismatch that can become problematic in periods of stress. If investors seek to withdraw, managers may be forced to delay redemptions or sell assets at discounted valuations, amplifying losses.

With superannuation funds increasingly exposed to private markets, ASIC is also concerned that stress in private credit could have broader system implications if large investors are forced to rebalance or raise liquidity quickly.

Where does this leave banks and private credit going forward?

The convergence of regulatory pressure, economic headwinds, and property market weakness is reshaping the outlook for both traditional banks and private credit providers. Banks are already responding through tighter lending, reduced competition for borrowers, and a focus on margins amid slower growth.

Private credit, meanwhile, faces a critical test. After years of expansion, the sector must demonstrate that it can manage credit risk, maintain transparency, and provide realistic valuations in a more challenging economic environment.

References

- The Australian Financial Review, “ASIC says private credit valuations are ‘lagging… economic reality,’” 18 June 2026

- The Australian Financial Review, “Private credit confronts its valuation dilemma,” 26 June 2026

- The Australian Financial Review, “Judo bank’s bad debts raise red flags on health of small business,” 25 June 2026

- The Australian Financial Review, “Westpac investor loans plunge one-fifth on federal budget tax shock,” 11 June 2026

- The Australian Financial Review, “Sydney, Melbourne price declines deepen in ‘glum’ housing market,” 1 July 2026