Why did the market fall?

The S&P 500 has officially entered a correction, down over 10% with more than $US5 trillion erased from the world’s leading market index. The fall means the market has given back all its gains since President Trump’s election victory on November 5th. As the president’s 25% tariffs on Canada and Mexico rattled investors fearing a resurgence in inflation, where companies could pass on higher import costs to consumers, and an economic growth slowdown as occurred after Trump’s tariffs in 2018. Trump has also stated another round of tariffs will be announced on April 2nd, creating further uncertainty for investors.

These declining outlooks for the US economy have been coupled with new fiscal spending commitments across Europe, as governments turbocharge defence and infrastructure spending, in a bid to sure up economic activity and national security amidst increasing trade and foreign policy tensions with the US. The move has been led by Germany, historically known for its frugal fiscal policy, which in March announced a €500 billion ($860 billion) defence spending package1.

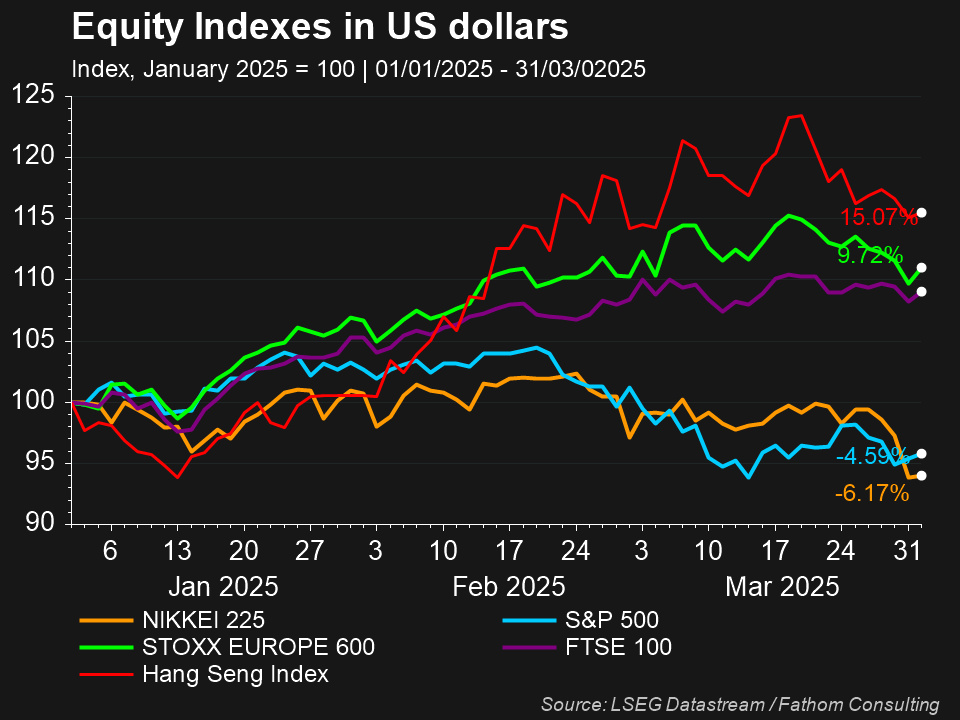

Investors have flocked to Europe, Asia, and emerging markets following these developments. The Stoxx 600 index, which comprises the largest listed companies in the UK and Europe, is up 9.7% this year, and the Hang Seng index, which includes some of Asia’s largest companies, is up 15%. The S&P 500 has, by comparison, declined over 10% since its February 19th peak, and 4.6% year to date. The large swings are consistent with Bank of America’s recent fund manager survey, which highlights managers now being on average 23% underweight US stocks, compared to 17% overweight in February2. As investors rotate their portfolios from US companies trading on high valuations with significant earnings growth priced in, to European and Asian stocks with less demanding valuations and now more rosy economic outlooks, following their governments’ new spending announcements.

What are the lessons for investors?

The market’s sudden rotation highlights the value of diversification for investors, and how being overly concentrated in stocks heavily linked to any one economy or sector can spell trouble when these do not perform as expected. Being more diversified allows investors to capitalise on a variety of growth opportunities, by purchasing assets like European and US stocks that perform differently across market conditions. Which helps build a more resilient portfolio that isn’t dependent on any one growth story playing out to achieve desired returns.

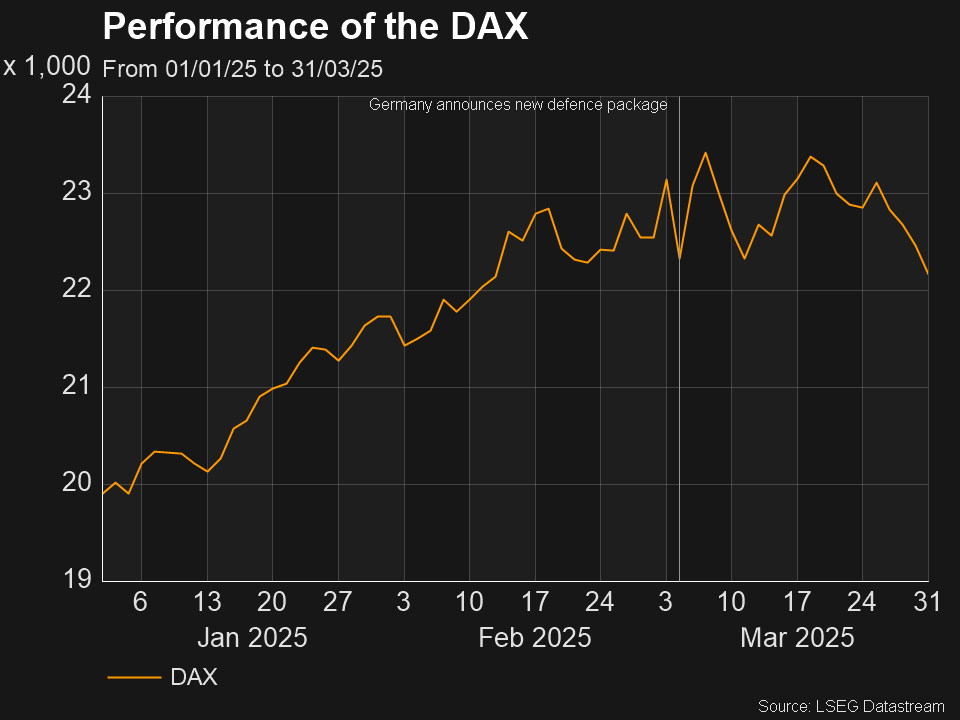

The spark for the market’s rotation, Trump tariffs being expected to slow US economic growth as European fiscal spending and growth picks up, demonstrates another valuable lesson for investors. Markets are forward looking, and everything known or expected about a company is already reflected in its stock price. Germany’s new €500 billion in defence spending is an example of this. As the package was unexpected, the German stock market (the DAX) reacted with a large swing in prices, reflecting investors adjusting their valuations for companies based on the spending’s anticipated impact. If the market had expected this announcement however, stock prices would likely not have reacted as significantly, due to the package’s anticipated impacts already being reflected in investors’ valuations.

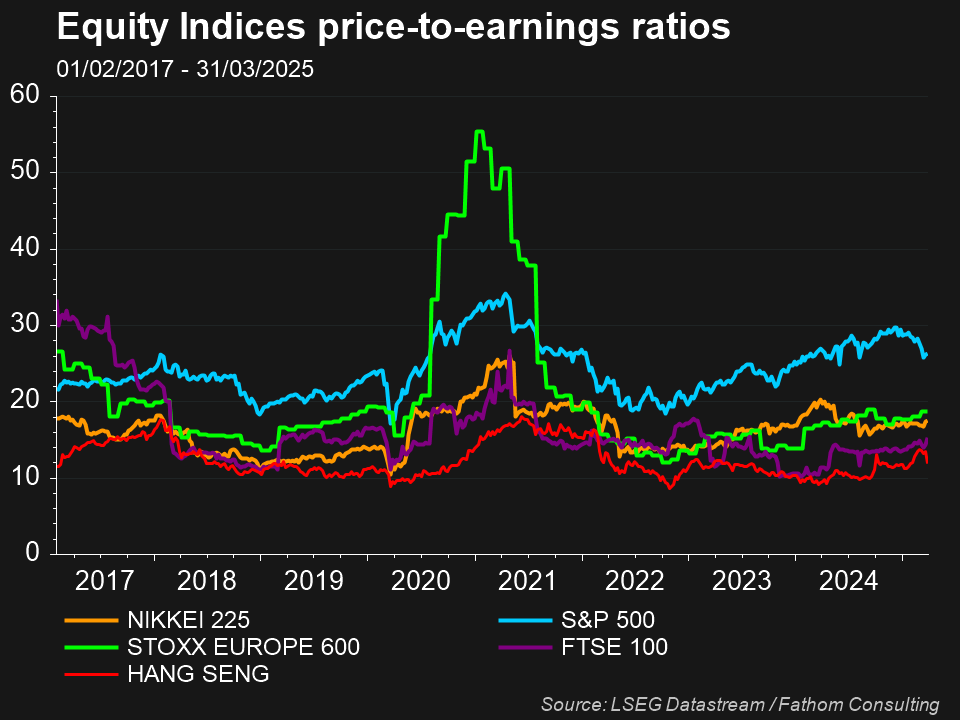

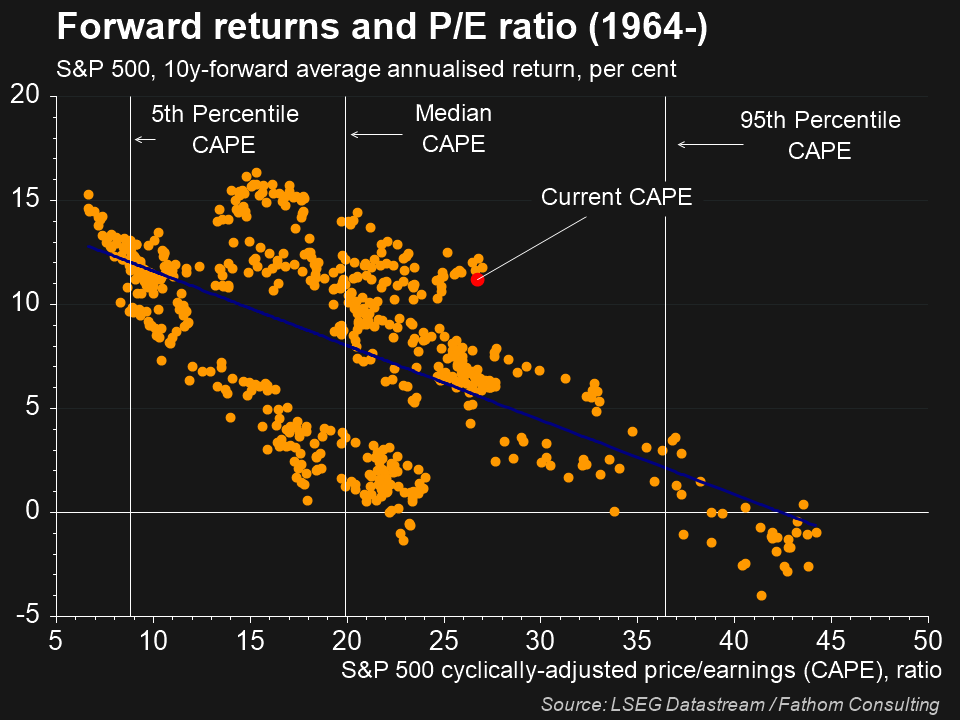

This efficiency in how the market quickly adjusts prices based on investor outlooks highlights how sentiment can drive market movements, as investors rush to buy or sell stocks based on adjustments to their valuations. This results in changes to stocks’ Price-to-Earnings ratios (P/Es), which expresses how much the market is willing to pay for a company’s current earnings. Investors will ascribe a company with greater expected earnings growth a higher P/E, as more of its profits are expected in the future and are not reflected in current figures. However, because these companies are being valued more heavily based on future profits, this introduces greater uncertainty to their valuations, as such profit expectations can quickly change, as has occurred in the US recently as investors cut profit forecasts based on unanticipated Trump tariffs taking effect.

What drives market gains is therefore earnings outperforming investors’ expectations. If stocks are trading on high P/E ratios relative to history, this can be used as a gauge for investor sentiment to highlight that significant earnings growth is being incorporated into valuations. Such an environment makes it more difficult for companies’ profits to outperform expectations, potentially leaving minimal room for positive earnings surprises that could suppress market gains.

The S&P 500’s high P/E relative to other international markets continues to make us weary of whether the market’s rotation will continue, as governments in Europe and Asia continue to announce new spending packages. Whatever the US market’s path from here, the recent correction highlights the value of a diversified portfolio for investors, and how excessively optimistic growth expectations can leave stocks vulnerable to swift price changes as market outlooks change.

References

- Australian Financial Review, “Why last night may reverberate on markets for decades,” March 19, 2025

- Australian Financial Review, “Investors are turning to the safest of assets for Trump-era security,” March 19, 2025