What are semiconductor stocks and why do they matter?

Semiconductor stocks, often referred to as chip stocks, represent companies that design, manufacture or supply the components that perform the core computing tasks inside digital systems. These chips handle calculations, move data and store information, making them essential to data centres, cloud computing and artificial intelligence (AI) models.

In the context of AI, semiconductors are particularly critical because training and running large models requires enormous computing power. Advanced processors perform the calculations, while high‑performance memory chips store and rapidly move vast amounts of data. As AI models grow more complex and are deployed at scale, demand for both processing and memory capacity rises sharply. This has turned semiconductors from a traditionally cyclical industry into one that many investors now view as structurally supported by long‑term capital spending.

Why is AI driving such strong demand for chips?

The current wave of AI investment is unprecedented in scale. Global technology giants are spending hundreds of billions of dollars building data centres filled with specialised chips to train and run AI models. These facilities require not just cutting‑edge processors, but also networking chips, advanced memory and sophisticated packaging technologies that allow multiple chips to work together efficiently.

Unlike previous technology cycles, AI workloads are both compute‑intensive and persistent. Once models are trained, they must still be run continuously to deliver services, which creates ongoing demand for chips rather than a one‑off burst of spending. This has encouraged customers to lock in supply years in advance, supporting revenues and margins across the semiconductor value chain.

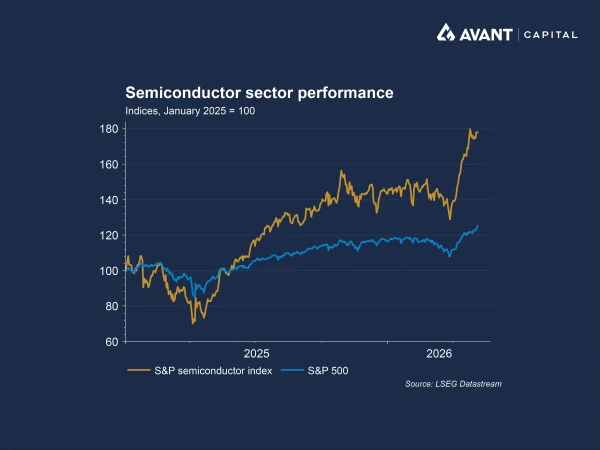

Why have semiconductor stocks surged so sharply?

With this backdrop, semiconductor stocks have rallied sharply as earnings expectations have been repeatedly revised higher. Chipmakers have reported robust order books, strong pricing power and improved visibility compared with past cycles. In some areas, particularly memory, tight supply has pushed prices higher and transformed what was once a volatile commodity business into a strategic bottleneck for AI infrastructure.

The rally has also been broad. Designers, manufacturers, equipment suppliers and memory producers have all benefited, reflecting how widespread the demand shock has been. As a result, semiconductors have become one of the dominant contributors to global equity market performance over the past year.

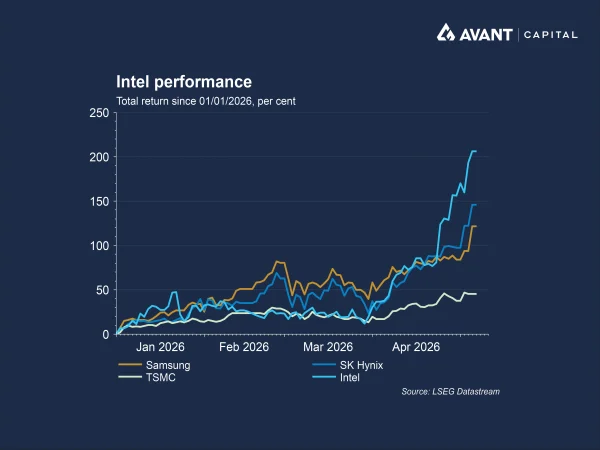

Why has Intel’s share price rebounded?

One of the more notable developments within the rally has been the resurgence of Intel. After years of underperformance and missed technological transitions, Intel has regained investor attention as AI workloads evolve. While much of the initial AI boom focused on specialised accelerators, newer applications, including AI “agents” and inference, rely more heavily on central processing units, an area where Intel remains strong.

Beyond demand dynamics, Intel’s strategic importance has increased as geopolitical risks have come into sharper focus. Taiwan produces more than 90% of the world’s most advanced semiconductors, leaving global technology supply chains heavily concentrated in a single location1. Governments are increasingly seeking to reduce this reliance, particularly for chips critical to AI, defence and digital infrastructure.

In this context, Intel’s US manufacturing footprint has gained renewed relevance. The company has received direct backing from the US government, including equity investment and support under industrial policy programmes designed to rebuild local chipmaking capacity. Alongside its push into advanced packaging, this positions Intel as a potential beneficiary of efforts to diversify semiconductor supply chains should tensions around Taiwan escalate.

Why has Samsung reached a $US1 trillion market value?

Samsung Electronics’ rise to a market capitalisation of $US1 trillion highlights another crucial pillar of the AI boom: memory2. AI systems are extraordinarily memory‑hungry, particularly for high‑bandwidth memory, which allows processors to access and move data at extreme speeds. Samsung, alongside South Korea’s SK Hynix and a small group of other suppliers, dominates this strategically important segment of the semiconductor market.

Demand for memory has surged as hyperscalers race to expand data centre capacity, pushing prices higher and driving a sharp rebound in profitability. Customers are increasingly locking in long‑term supply agreements to secure access, reinforcing the view that memory is no longer a purely cyclical product. Instead, investors are beginning to see it as core AI infrastructure, essential to sustaining model training and deployment at scale. This shift in perception has played a significant role in Samsung’s re‑rating, with similar dynamics underpinning the sharp rise in SK Hynix’s valuation.

What does this mean for EM and DM diversification?

The dominance of memory and logic chipmakers in the AI supply chain has helped reshape global equity markets. In emerging markets, a small number of Asian chipmakers, including Samsung, SK Hynix and Taiwan Semiconductor Manufacturing Company, now account for a substantial share of market indices. This concentration has reduced the diversification benefits that investors have traditionally sought from emerging market equities.

Developed markets face related challenges. Semiconductor stocks are closely tied to the same AI‑driven capital spending cycle that is powering US technology giants, increasing correlations across regions. As a result, both emerging and developed market portfolios have become more exposed to a single investment theme, raising questions about resilience should sentiment towards AI spending weaken or capital expenditure slow.

What risks could derail the rally?

Despite strong fundamentals, risks remain and valuations are high. AI capital spending could slow if economic conditions weaken or if returns on investment disappoint. Rapid capacity expansion could eventually lead to oversupply, particularly in memory.

Given the semiconductor sector represents a material share of S&P 500 market capitalisation, any earnings disappointment in parts of the sector that already assume sustained growth could leave semiconductor stocks and the broader market vulnerable if demand falls short of expectations.

References

- Financial Times, “The chips chokehold that could end the AI investment boom,” 10 April 2026

- The Wall Street Journal, “Samsung’s market value hits $1 trillion,” 6 May 2026