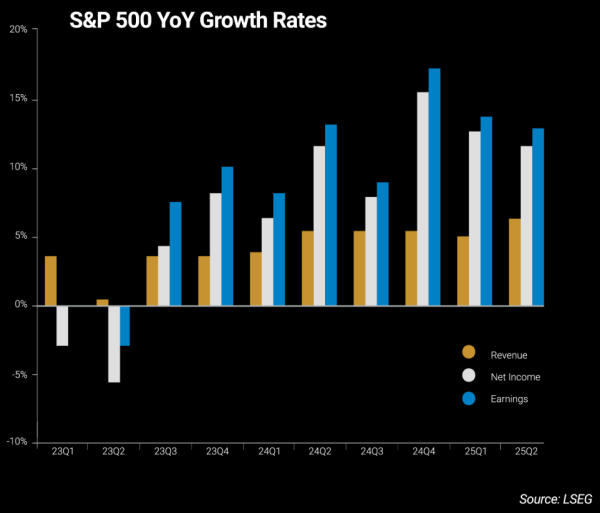

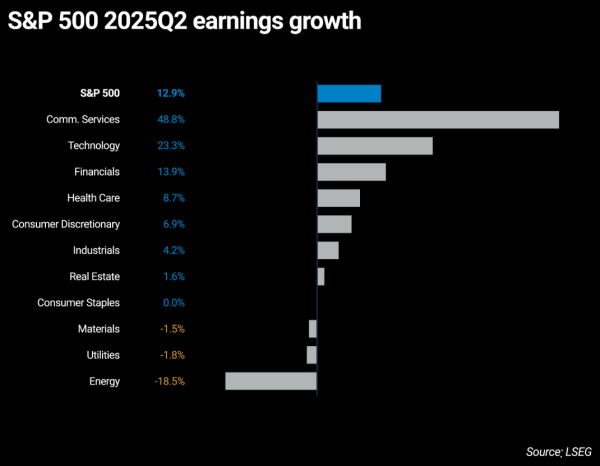

US corporate profits in the second quarter (Q2) of 2025 have proven resilient, with the S&P 500 reporting 12.9% earnings growth and 80% of results exceeding investor expectations1. However, results revealed a widening divide in performance, driven by strong growth in technology firms and lagging growth in the consumer discretionary sector. While headline figures suggest resilience, the underlying data paints a more nuanced picture of economic momentum and margin pressure.

What have been the best performers?

Mega-cap technology firms—Apple, Microsoft, Meta, and Alphabet—once again delivered standout results2. The tech and communication services sectors posted earnings growth of 23.3% and 48.8%, respectively, with Microsoft and Meta reporting 25% and 36% increases, driven by AI monetization and robust cloud services demand. Financials also performed well, supported by a steepening yield curve, deregulation, and high asset market trading volumes, resulting in 13.9% earnings growth.

What about everyone else?

Beyond Wall Street and Silicon Valley, many sectors are grappling with the impact of President Trump’s renewed tariff regime. Consumer discretionary, staples, and industrials reported more subdued earnings growth of 6.9%, 0%, and 4.2%, respectively. Carmakers and appliance manufacturers—directly exposed to tariffs—dragged down sector performance with significant downward profit revisions. Energy was the biggest laggard, reporting an 18.5% earnings decline due to falling oil prices.

While the headline impact of tariffs on Q2 results was muted, Wall Street had already revised expectations downward heading into earnings season. JPMorgan notes that earnings-per-share estimates for Q2 were cut by 4% between April and June, meaning many companies beat expectations only because the bar had been lowered3.

How has consumer spending held up?

Consumer demand remains relatively resilient, with Q2 consumption in the US growing 1.4% quarter-on-quarter, up from 0.5% in Q1. However, spending patterns are evolving. Discretionary categories such as health and personal care are outperforming big-ticket items like electronics and appliances, which consumers appear to be postponing. Companies are cautiously raising prices but remain wary of demand destruction, especially given low consumer confidence and lingering inflation fatigue from 2022.

What about profit growth concentration?

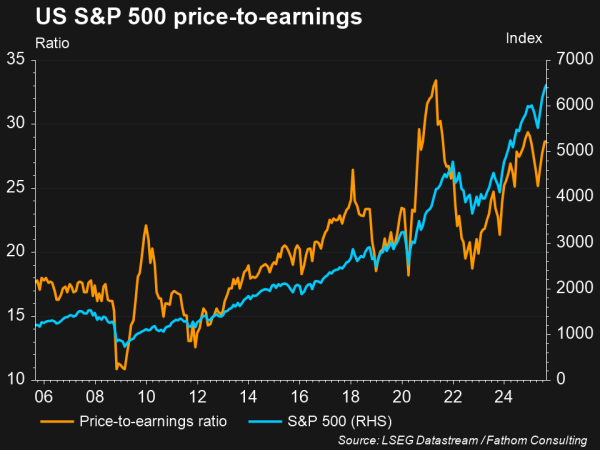

The concentration of profit growth in a handful of tech giants has raised concerns for some investors, as the broader S&P 500 continues to climb despite subdued growth in retail and industrial sectors4. The index’s returns have therefore been heavily driven by valuation expansion, with the index’s price-to-earnings ratio continuing to rise as investors justify current valuations with expectations for high future earnings growth.

Whether these expectations are overly bullish or bearish remains to be seen, and, like Q2 earnings season, will depend heavily on the mega-cap tech companies’ ability to continue their stellar growth.

References

- London Stock Exchange Group, “S&P 500 earnings scorecard,” 22 August 2025

- Financial Times, “Without tech, where’s the profit growth?” 6 August 2025

- JPMorgan Asset Management, “US 2Q25 earnings update: Batten down the hatches,” 12 August 2025

- Financial Times, “Corporate profits are slowing,” 5 August 2025