The opening months of 2026 have been marked by a clear divergence in market behaviour: major equity indexes have held relatively steady, even as many individual stocks have undergone pronounced and rapid swings in valuation. Much of this underlying volatility reflects how investors are responding to the growing influence of artificial intelligence, which is reshaping expectations around business model durability, earnings reliability and sector vulnerability. Understanding this widening gap between stable indexes and volatile constituents requires looking beyond headline performance and examining how investors are reassessing risk in an environment increasingly shaped by technological disruption.

What is causing such intense dispersion beneath a flat market index?

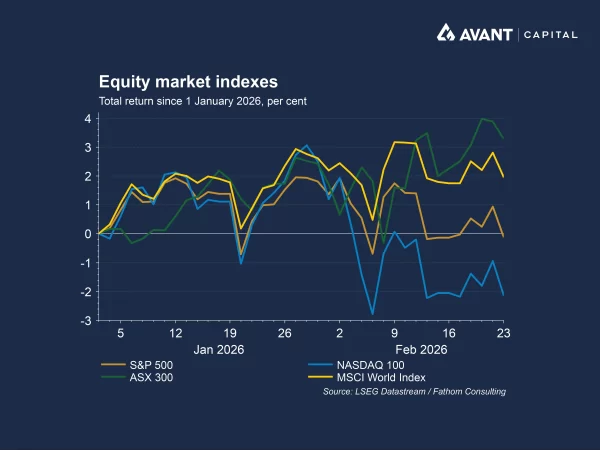

Although the S&P 500 has been broadly flat year‑to‑date, more than one‑fifth of its constituents have risen or fallen by over 20 percent in the same period, marking the widest gap between individual‑stock volatility and index calm since the aftermath of the global financial crisis1. This dispersion reflects a market undergoing significant internal repricing as investors confront the implications of AI on a sector‑by‑sector basis. The stability of the overall index masks the reality that capital is flowing rapidly between industries depending on how vulnerable businesses appear to AI automation.

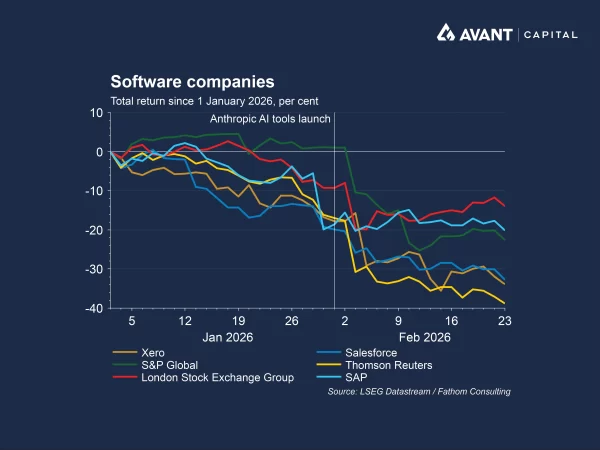

Artificial intelligence has triggered some of the sharpest reactions. When Anthropic announced tools capable of automating certain legal and research tasks in late January, approximately $US300 billion was wiped from software, financial‑data and exchange operators almost instantly2. This type of swift revaluation, driven by perceived technological threat, has become increasingly common. It underscores how fragile sentiment can be in areas where AI may alter operating models, cost structures or competitive dynamics. Meanwhile, capital has been rotating toward companies whose functions rest on physical assets or real‑world delivery, where AI cannot readily displace the value chain.

Why are earnings strong yet the index still lacking direction?

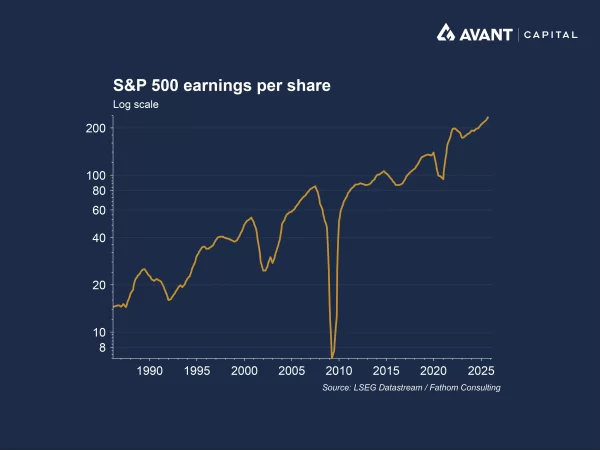

One of the most striking features of the current environment is that the volatility is not a result of weak fundamentals. On the contrary, earnings for the S&P 500 grew 12 percent year‑on‑year in the most recent quarter, marking the fourth consecutive period of double‑digit expansion.

The lack of broad index excitement stems partly from underperformance among the large technology companies that previously drove market returns. The Magnificent Seven have fallen more than 5 percent since January, overshadowed by concerns about heavy AI‑related spending and uncertainty about the long‑term profitability of these investments. Their muted performance has constrained index‑level gains, even as many smaller and mid‑sized companies post strong results.

How is AI shaping sector‑level winners and losers?

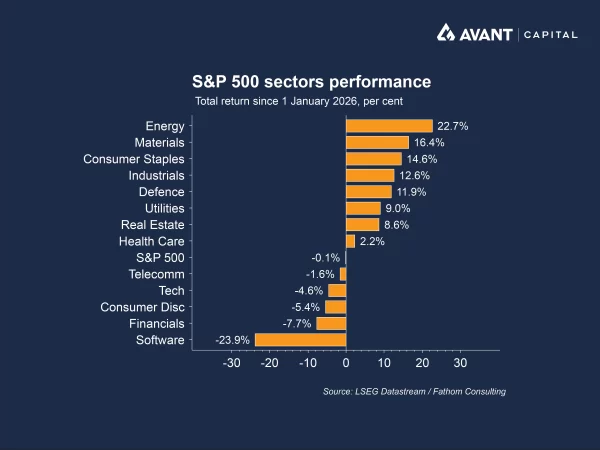

AI has introduced a new dimension to sector rotation, influencing not just performance but investor psychology. Sectors perceived as more insulated from AI, such as industrials, consumer staples, materials and utilities, have outpaced the index. These areas benefit from physical assets and operational activities that AI cannot easily replicate. Meanwhile, industries such as software, wealth management, insurance brokerage and commercial real estate have faced mounting pressure, driven by fears that AI could reshape workflows, client servicing, underwriting processes or pricing models.

This dynamic has also created notable divergence within industries themselves. Delta Air Lines, for example, has risen more than five percent in February, while online travel platform Expedia has fallen over twenty percent in the same period. The contrast reflects differing levels of AI exposure. AI can help travellers find cheaper flights but cannot replace the necessity of aircraft fleets, aviation infrastructure or the physical act of flying. By contrast, online travel platforms operate in the digital realm, where AI‑enhanced competition could intensify and compress margins. This example illustrates how the market is drawing sharper distinctions between asset‑dependent operators and digital intermediaries.

Why are active managers finding new opportunities in this environment?

For the first time in nearly two decades, more than half of large‑cap mutual funds are outperforming their benchmarks, a reversal from years in which passive strategies dominated. This shift is largely driven by the breadth of stock performance: more than 60 percent of S&P 500 constituents have outperformed the index this year. With mega‑cap technology names no longer the sole drivers of returns, active managers are finding opportunities in identifying companies with clearer earnings momentum, stronger business model durability or reduced exposure to AI disruption.

What will determine whether this pattern continues?

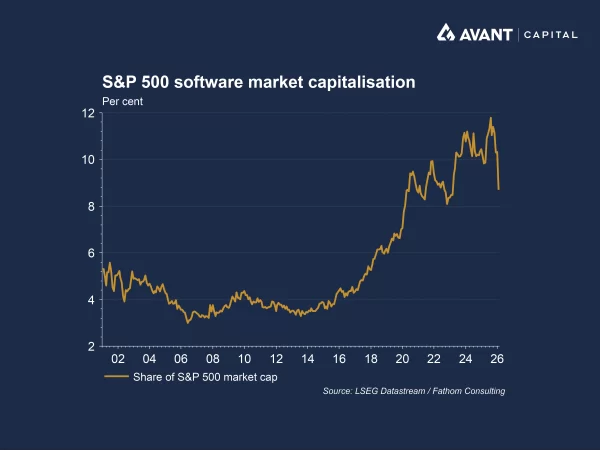

The sustainability of this divergence will depend on a combination of corporate earnings, market psychology and the next developments in AI. What is increasingly clear is that investors are entering a new phase of AI‑era market behaviour. The exuberance of prior years has given way to a more measured, scrutinising approach that distinguishes between genuine resilience and speculative promise. Indexes may appear calm, but the turbulence beneath the surface reflects a market actively reshaping itself to the realities of technological disruption, and risks could build further if weakness in software persists given the sector’s large weighting and influence within the S&P 500.

References

- Financial Times, “Earnings and AI fears drive ‘extreme’ churn in US stock market,” 22 February 2025

- The Wall Street Journal, “Wall Street’s latest bet is on ‘HALO’ companies with AI immunity,” 22 February 2026