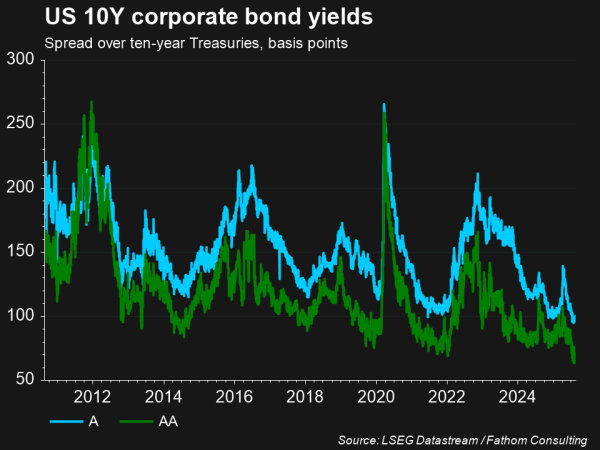

What’s been happening with US credit spreads?

US credit spreads—the gap between US companies’ borrowing costs and US Treasury yields—have tightened to their lowest levels in over a decade1. Credit spreads serve as a proxy for default risk, indicating how much additional yield investors demand for holding corporate bonds over risk-free government bonds. These yields move inversely to bond prices, meaning higher prices result in lower yields.

The recent tightening has been driven by strong demand for US credit. A series of trade agreements and robust earnings on Wall Street have lifted market expectations for economic growth. As a result, investors have assigned lower default risk to corporate issuers, increasing demand for credit, which pushes up bond prices and, in turn, lowers yields.

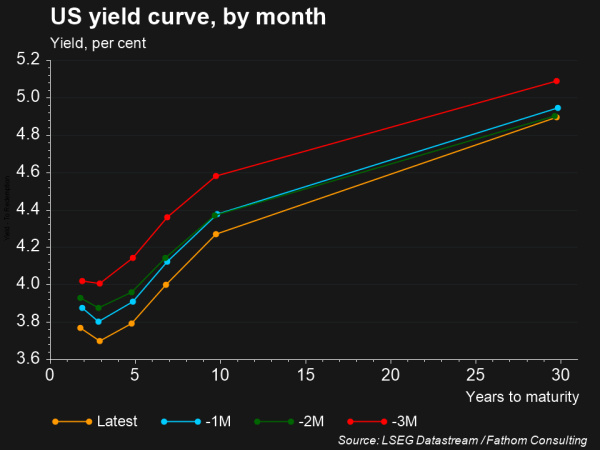

Simultaneously, weaker jobs data in recent months has raised expectations for interest rate cuts by the US Federal Reserve, as the central bank aims to prevent a further slowdown in employment. This has led to a decline in US Treasury yields, while corporate bond yields have also fallen—driven by increased investor demand for higher returns, which pushes up credit prices. As a result, the spread between government and corporate bond yields has narrowed further.

What are the risks from tight credit spreads?

Some investors have warned that such tight credit spreads may reflect excessive optimism about the US economy, potentially underestimating the risk of corporate defaults—particularly as tariffs rise to their highest levels in decades. While credit spreads suggest stability, markets are also pricing in multiple rate cuts by the Federal Reserve, signalling concerns about a potential economic slowdown.

Other investors, however, argue that current spreads are justified due to strong corporate balance sheets, which they believe reflect solid fundamentals and low default risk.

How have companies responded?

US companies have capitalised on these tight spreads—and the opportunity to raise capital at a relatively modest premium over US Treasury yields—by issuing a record volume of highly rated debt. In the first half of 2025 alone, $910 billion in investment-grade bonds were issued, marking the second-highest total on record. This surge reflects both investor appetite for yield, and corporate efforts to take advantage of favourable credit conditions amid an uncertain economic backdrop.

The sustainability of these tight credit spreads will depend on how inflation and economic growth evolve, and whether investors begin to assign more or less default risk to companies. The trajectory of Federal Reserve interest rate cuts will also be closely monitored, as it will influence both Treasury yields and broader perceptions of economic stability.

References

- Financial Times, “US credit spreads hit lowest level this century after sharp rally,” 21 August 2025