How strong is the overall earnings backdrop?

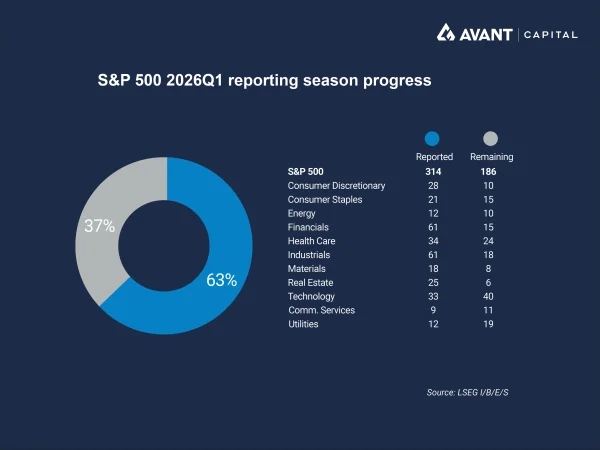

The US first‑quarter 2026 earnings season has so far reinforced the message that American corporate profits continue to outperform expectations, even amid a complex macroeconomic and geopolitical backdrop. With results reported by around two‑thirds of S&P 500 companies, early aggregate outcomes point to a solid start to the season, with earnings growth running comfortably ahead of long‑run averages and a high proportion of firms beating consensus forecasts.

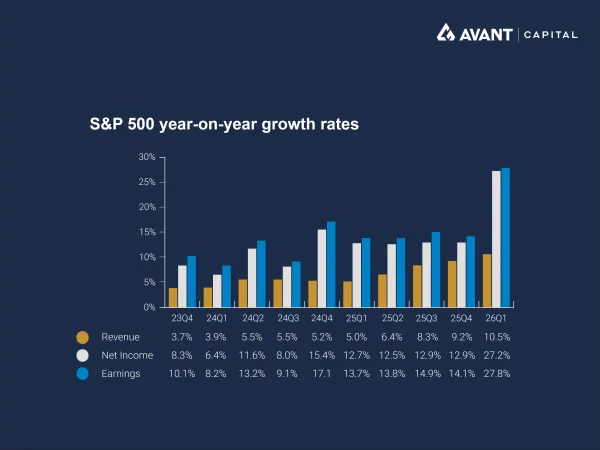

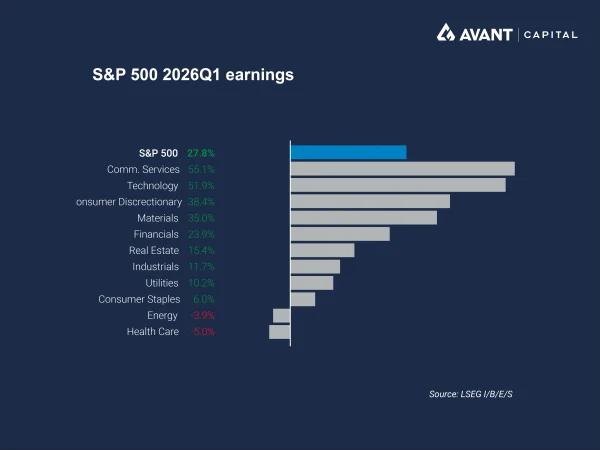

According to LSEG I/B/E/S data, S&P 500 earnings are up around 27.8% year on year for the March quarter based on results reported to date, with more than 80% of reporting companies exceeding analyst estimates, well above the long‑term average beat rate1.

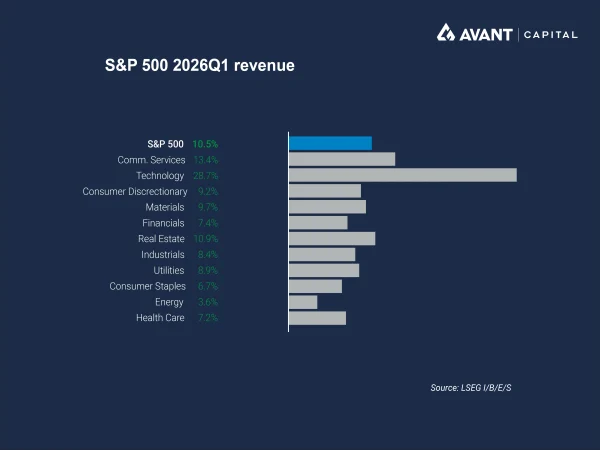

Revenue growth has also been robust, rising close to 10% year on year, suggesting that profit strength has not been purely cost‑driven but underpinned by genuine top‑line momentum.

That said, these results should be interpreted as an early read rather than a definitive assessment of the quarter. The reporting cohort to date has been weighted towards sectors that have delivered strong earnings momentum in recent periods, notably technology and financials, raising the possibility that aggregate growth rates could moderate as more cyclical and defensive sectors report.

Even so, the resilience shown so far is notable given tighter financial conditions, elevated interest rates and rising geopolitical risk. US corporates continue to demonstrate pricing power, operational discipline and an ability to navigate supply‑chain and labour‑market pressures. While some cyclical sectors have delivered more mixed outcomes, the early tone of the season has been one of earnings durability rather than clear late‑cycle stress.

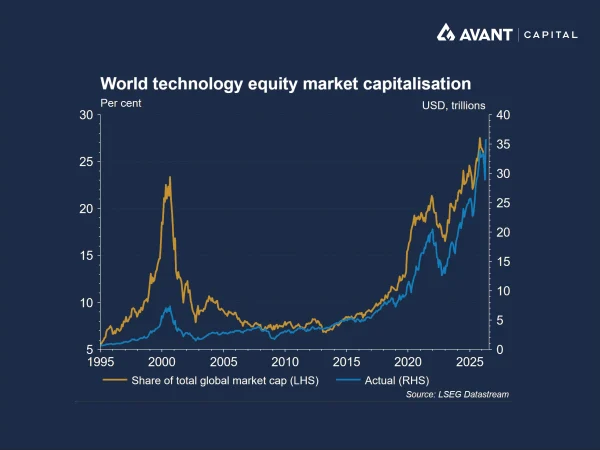

Why has the technology sector once again dominated profit growth?

As in recent quarters, the technology sector has been the standout contributor to earnings growth among companies that have reported so far. The sector has delivered 51.9% year‑on‑year earnings growth, far outpacing the broader market and accounting for a disproportionate share of aggregate profit expansion. Communication services, heavily influenced by digital advertising and platform economics, have also posted solid gains.

Big Tech earnings have underscored this divergence. Microsoft, Alphabet, Amazon and Meta have collectively reported strong revenue growth, expanding margins and accelerating demand tied to cloud computing and artificial intelligence. Microsoft has delivered double‑digit revenue growth, with Azure cloud revenues rising around 40% year on year, reflecting continued enterprise investment in AI‑enabled infrastructure2. Alphabet has reported an 81% surge in net income, driven by a rebound in advertising and explosive growth in Google Cloud, where revenues have risen by 63% year on year3. Amazon’s AWS business has also re‑accelerated, while Meta has delivered its strongest revenue growth in years as advertising monetisation has improved4.

While these results highlight the continued earnings power of large‑cap technology, they also reinforce the extent to which early‑season earnings strength has been concentrated in a relatively narrow group of market leaders.

What role is AI spending playing in current results?

A defining feature of this earnings season has been the sheer scale of ongoing AI‑related capital expenditure. Major US technology platforms have reiterated or lifted already ambitious investment plans, with combined 2026 capex running into the hundreds of billions of dollars. Microsoft, Alphabet, Amazon and Meta have all highlighted rising spending on data centres, proprietary chips and cloud infrastructure to support AI training and inference workloads.

However, the scale of this investment has also sharpened investor scrutiny. While companies have stressed the long‑term strategic importance of building AI capacity, markets have remained focused on near‑term returns. Meta’s shares, for example, came under pressure after the company flagged higher‑than‑expected capital spending, underscoring concerns around capital discipline, margin dilution and the timing of pay‑offs from AI investment.

Management teams have nevertheless emphasised that AI spending is increasingly translating into revenue growth rather than remaining purely speculative. Cloud backlogs have expanded sharply, AI‑enhanced products have gained traction and enterprise customers have continued to commit to long‑dated contracts. Even so, margins are being pressured in the short term by higher depreciation, energy costs and infrastructure operating expenses. Companies argue that scale, utilisation and productivity gains should ultimately support longer‑term profitability, but the path to that outcome remains uneven.

This dynamic has introduced an element of delayed gratification for investors, with much of the expected value from AI investment lying several years into the future. While early first‑quarter results point to emerging signs of monetisation, market reactions suggest confidence will depend on clearer evidence that today’s elevated spending can deliver sustainable returns.

How supportive is the domestic policy environment?

Beyond company‑specific drivers, the policy backdrop may offer potential tailwinds for US corporates. President Trump’s so‑called “big, beautiful bill”, which includes tax cuts and fiscal incentives, alongside banking deregulation, could support business confidence, credit availability and capital investment over time. Financials have posted solid earnings growth in the first quarter to date, reflecting higher net interest margins and stable credit conditions.

While the precise economic impact of these policy initiatives remains uncertain, they contribute to a broader narrative of relative US exceptionalism compared with other developed markets facing weaker growth and more constrained fiscal settings.

What about the war in Iran?

Despite encouraging backward‑looking results, forward guidance has struck a more cautious tone. Management commentary has frequently referenced heightened uncertainty around geopolitics, energy prices and interest rates. The war in Iran and disruption to the Strait of Hormuz have emerged as material macro concerns, with oil prices rising sharply during the earnings period. Any prolonged closure of this critical shipping route could weigh on global growth while simultaneously pushing inflation higher.

Such an outcome would complicate the Federal Reserve’s task. Higher energy‑driven inflation raises the risk that policy rates remain “higher for longer”, tightening financial conditions just as companies ramp up capital spending. Several firms have flagged rising input and transportation costs, highlighting the sensitivity of margins to further commodity‑price shocks.

What does this earnings season ultimately tell us so far?

Taken together, the early phase of the first‑quarter 2026 earnings season suggests that US corporate profits, led by Big Tech, remain in strong shape and continue to outperform global peers. AI‑driven investment is reshaping balance sheets and income statements, with early signs of revenue leverage emerging.

However, with more than a third of companies still yet to report, risks remain around the breadth and sustainability of earnings. Elevated valuations, sector concentration, and geopolitical risks, including the ongoing disruption in the Strait of Hormuz, leave markets increasingly sensitive to shifts in growth assumptions and broader macro conditions as the earnings season progresses.

References

- LSEG I/B/E/S, “S&P 500 earnings scorecard,” 1 May 2026

- The Wall Street Journal, “Microsoft reports strong cloud growth, but questions about AI returns persist,” 29 April 2026

- The Wall Street Journal, “Google profit jumps 81% as cloud business booms,” 29 April 2026

- Financial Times, “Tech earnings live: Google and Meta boost AI spending forecasts,” 30 April 2026