Kevin Warsh’s confirmation hearing to become the next chair of the US Federal Reserve was one of the most closely watched central banking events in years. Coming amid heightened political pressure on the Fed, elevated inflation driven partly by the Iran conflict, and renewed scrutiny of the central bank’s post‑pandemic actions, Warsh’s testimony offered important clues about how he sees the institution’s role, limits and priorities. While he spoke frequently about reform and “regime change,” his remarks suggested evolution rather than abrupt upheaval, particularly on interest rates and the Fed’s balance sheet1.

How did Warsh frame the issue of Federal Reserve independence?

A central theme of the hearing was Fed independence, an issue thrust into the spotlight by President Donald Trump’s repeated public demands for rate cuts and the ongoing Department of Justice investigation into current chair Jay Powell. Warsh argued that the operational independence of monetary policy was not “particularly threatened” when elected officials express views on interest rates, describing such pressure as a long‑standing feature of US political life2.

What did Warsh say about interest rates and near‑term policy signals?

Despite market sensitivity around the prospect of rapid rate cuts, Warsh offered little concrete guidance on the future path of interest rates. He firmly denied that President Trump had asked him to commit to any rate decisions during the nomination process, saying he would never agree to do so. Throughout the hearing, he resisted calls to provide forward guidance, criticising the Fed’s existing practice of signalling future policy through dot plots.

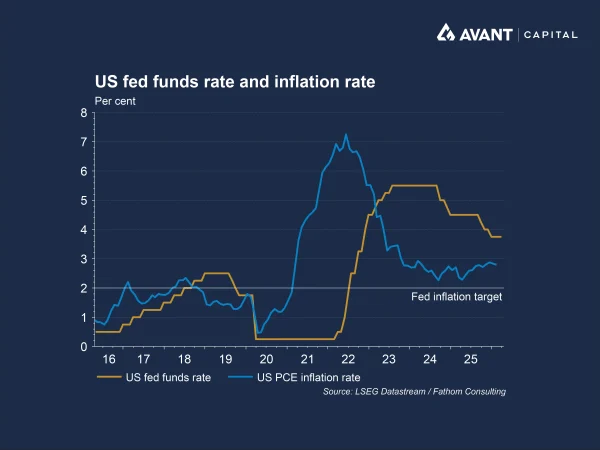

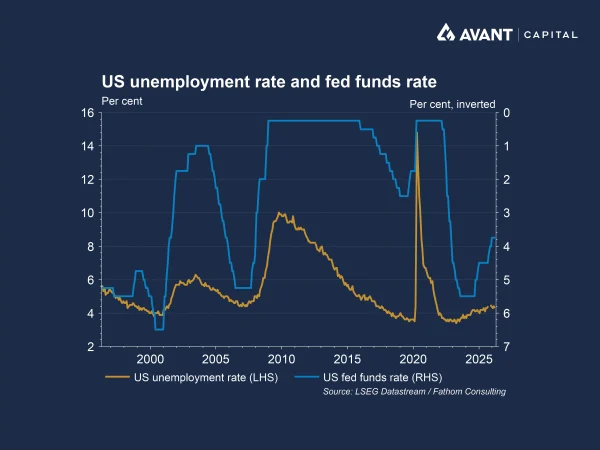

Warsh argued that interest rates should remain the primary tool of monetary policy in normal times, rather than the balance sheet. However, he stopped short of endorsing imminent easing. His remarks suggested caution, particularly given inflation remains above the Fed’s 2 per cent target and energy prices have surged following the Iran conflict. While Warsh has previously argued that productivity gains from artificial intelligence could ultimately lower inflation, during the hearing he was careful not to link that view explicitly to near‑term rate cuts.

How does Warsh view inflation and the Fed’s policy framework?

Warsh returned repeatedly to the idea that “inflation is a choice,” a phrase he has used in past writings and speeches. He argued that inflation reflects policy errors, particularly excessive money creation and delayed responses to rising prices in the aftermath of the pandemic. In his opening remarks, he placed greater emphasis on price stability than on the Fed’s employment mandate, signalling a desire to rebalance priorities.

He also questioned the data used to assess underlying inflation, criticising the Fed’s reliance on core personal consumption expenditure measures. Warsh suggested greater use of alternative indicators such as trimmed mean and median inflation. While these ideas represent a shift in emphasis rather than a wholesale break, they point to potential changes in how inflation risks are assessed and communicated under his leadership.

What is Warsh’s stance on the Fed’s balance sheet and quantitative easing?

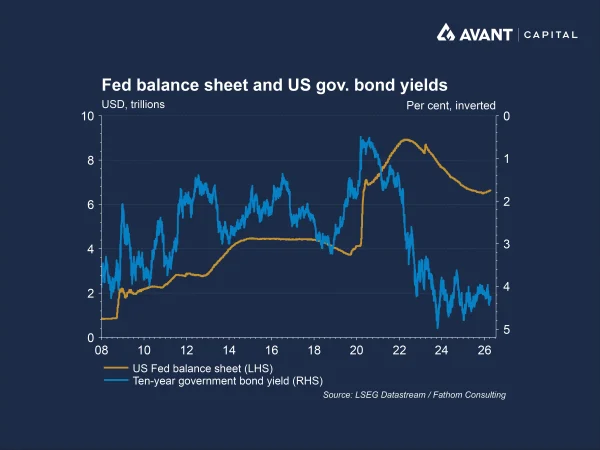

Perhaps the clearest area of conviction in Warsh’s testimony was his criticism of the Fed’s large balance sheet. He described successive rounds of quantitative easing as “fiscal policy in disguise,” arguing that large‑scale bond purchases have distorted financial markets and blurred the boundary between monetary and fiscal policy. Warsh said the balance sheet had become an “ordinary, recurring force” rather than an emergency tool, a development he views as unhealthy.

That said, Warsh was careful to stress that any effort to shrink the balance sheet should be gradual and predictable. He acknowledged that it took many years to expand the balance sheet and that it would not be unwound quickly. He suggested that interest rate policy and balance sheet policy should work together, rather than one substituting for the other, and hinted that closer coordination with the US Treasury may be required to achieve a smaller footprint without destabilising markets.

What could this mean for bond markets and longer‑term yields?

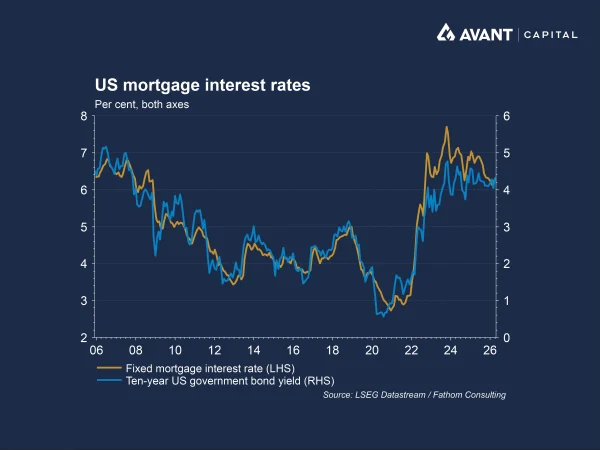

Although Warsh avoided explicit market guidance, his emphasis on balance sheet reduction carries potential implications for bond markets over time. A smaller Fed footprint could mean greater reliance on private demand to absorb Treasury issuance, which in theory may place upward pressure on longer‑dated yields. Since mortgage rates tend to track movements in the 10‑year Treasury, any sustained rise in long‑term yields could feed through into higher housing‑market borrowing costs and, by extension, slower economic activity. However, his insistence on gradualism suggests an awareness of the risks of disrupting the Treasury market or triggering volatility in funding conditions.

Market reactions during the hearing reflected this tension. US Treasury yields edged slightly higher as Warsh reiterated his commitment to reform while resisting calls for immediate easing, highlighting how closely investors are watching for any change in the Fed’s policy approach. Importantly, his comments suggested a preference for gradual, carefully signalled adjustments rather than abrupt shifts in policy.

Is a Warsh‑and‑reset coming to the Fed?

Warsh repeatedly used the language of “regime change”, but his testimony suggested a reform agenda that is more methodical than radical. He outlined ambitions to rethink the Fed’s inflation framework, improve communication, reduce reliance on forward guidance and gradually shrink the balance sheet. Yet he also emphasised predictability, internal debate and respect for institutional constraints.

Taken together, Warsh’s confirmation hearing painted a picture of a prospective Fed chair intent on reshaping the institution’s philosophy and scope, while avoiding abrupt policy shocks. For markets and policymakers alike, the key takeaway was not an imminent shift in rates, but a longer‑term re‑examination of how the world’s most influential central bank defines its role.

References

- Financial Times, “Warsh signals evolution, not revolution at the Fed,” 22 April 2026

- Financial Times, “Federal Reserve hearing as it happened: Senators grill Federal Reserve chair nominee Kevin Warsh on independence from Donald Trump and personal wealth,” 22 April 2026