Why has the immediate oil shock been less severe than feared?

The escalation in tensions involving Iran and the disruption to energy flows through the Middle East initially raised fears of a sharp and sustained spike in oil prices. The Strait of Hormuz is a critical artery for global energy markets, with a significant share of the world’s crude oil and refined products passing through it. Despite the gravity of the disruption, oil prices have risen less sharply than many had expected, and the immediate impact on physical supply has also remained relatively contained. A combination of emergency stockpiles, altered trade flows and demand-side adjustments has, at least temporarily, cushioned the blow.

A key reason is timing. Oil shipped from the Gulf can take up to 45 days to reach consuming nations1. As a result, markets have only gradually begun to feel the absence of barrels that would normally transit the region. In the early stages of the conflict, tankers that departed before hostilities intensified continued to arrive at their destinations, delaying the point at which shortages became visible in inventories and at the pump.

How have strategic oil reserves absorbed the initial shock?

Strategic and commercial oil reserves have played a central role in buffering the disruption. Governments across Asia, Europe and North America have drawn down stockpiles built up over recent years, partly in response to earlier energy shocks. These reserves have acted as a shock absorber, smoothing consumption even as new supply was constrained.

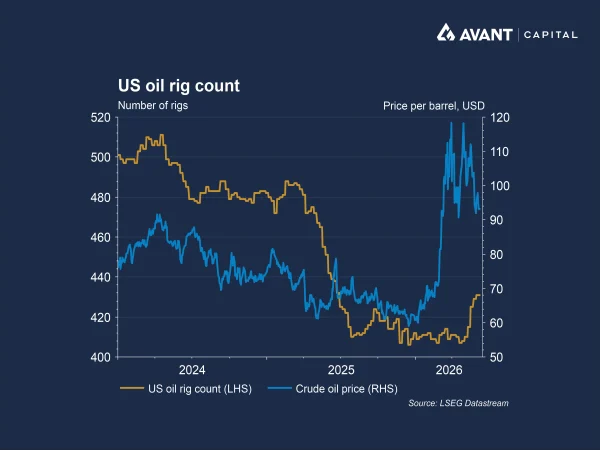

Higher prices have prompted some supply response outside the Middle East, particularly in the United States, where the oil rig count has begun to rise. However, this response remains incremental and insufficient to offset the scale of lost supply from the Gulf, reinforcing the market’s continued reliance on inventories and spare capacity elsewhere.

However, this cushion is thinner than it appears. According to analysis cited by Goldman Sachs, average oil stocks in several Asian economies, excluding China, cover only around a month of demand. Once inventories fall below critical levels, the market’s ability to absorb further disruption diminishes rapidly. This has already prompted governments to encourage demand containment measures, such as remote working, limits on air conditioning and reduced fuel subsidies, particularly in countries most dependent on Gulf supplies.

What role has China played in stabilising the market?

China has been a significant, if understated, stabilising force. With some of the largest strategic petroleum reserves in the world and greater flexibility over import and export flows, China has been better positioned than many peers to manage the disruption2. By relying more heavily on its own stockpiles and adjusting refinery runs, China has been able to reduce its immediate call on seaborne crude, easing pressure on global markets.

Why doesn’t reopening the Strait mean an instant recovery?

Even if the Strait of Hormuz were to reopen fully, supply would not snap back overnight. There is a substantial backlog of tankers, estimated at around 100 million barrels of oil, waiting to clear the strait3. Beyond the physical congestion, there is a behavioural lag. Shipping companies, insurers and traders need time to feel confident that risks have genuinely receded before resuming normal traffic patterns.

Industry leaders suggest this recovery could be measured in months rather than weeks. Executives from major Middle Eastern producers have indicated that it could take several months for traffic to return to 80% of pre-conflict levels, with a full normalisation potentially stretching into 2027. This implies that even a political resolution would leave the oil market structurally tight for an extended period. This is particularly significant for large net oil‑importing economies, which remain highly exposed to elevated prices and the associated pass‑through into inflation and growth, even if supply disruptions prove temporary.

What happens as reserves begin to dwindle?

As strategic and commercial reserves are drawn down, the market’s vulnerability increases. S&P Global Energy estimates that close to 500 million barrels of crude and refined products are needed to replenish inventories already used outside the Persian Gulf, a figure that rises by 5.8 million barrels for every day the strait remains closed. Even under optimistic assumptions of a supply surplus, rebuilding stocks to pre-war levels could take more than a year.

This dynamic creates an important feedback loop. Governments, scarred by repeated energy shocks, are now racing not only to refill reserves but to build larger buffers than before. While this may reduce future vulnerability, it also keeps near-term demand elevated, contributing to persistently higher oil prices.

How could higher oil prices affect markets and inflation?

The risk is that sustained higher energy prices begin to flow through to corporate margins and consumer inflation. Equity markets in many regions are trading near record highs, often reflecting optimism about earnings resilience and eventual monetary easing. A prolonged oil shock challenges this narrative. Higher input costs can compress margins, particularly in energy-intensive sectors, while elevated fuel prices act as a tax on consumers.

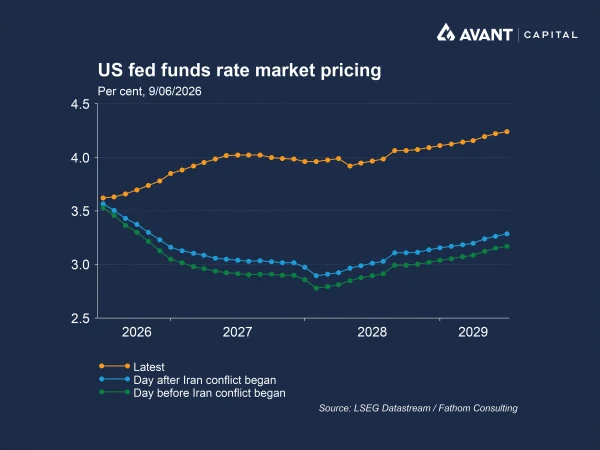

There is also a macroeconomic dimension. If higher oil prices feed into broader inflation expectations, central banks may be forced to keep policy tighter for longer, or even consider renewed rate hikes. This would mark a sharp reversal from the prevailing assumption that the next move in rates is down. In such an environment, the disconnect between asset prices and underlying economic fundamentals could narrow abruptly.

Why does this episode matter beyond the immediate crisis?

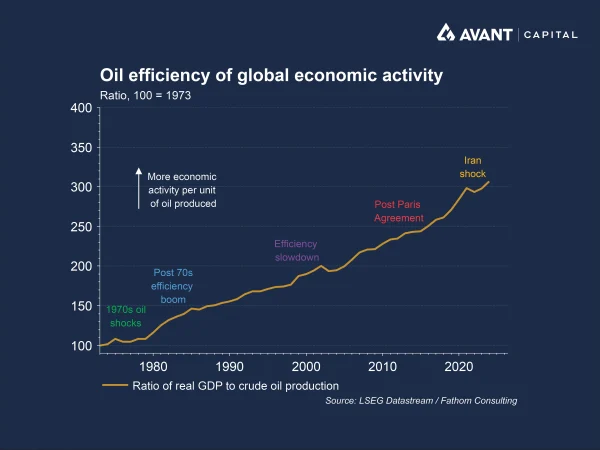

The Iran-related disruption underscores how fragile the global energy system remains. While the global economy is far more oil‑efficient than during previous supply shocks, it remains vulnerable to large, sudden and unprecedented losses of supply, particularly from geopolitically sensitive regions.

Reserves, alternative supply routes and demand adjustments can cushion shocks, but only temporarily. As buffers are depleted and rebuilding them takes time, the risk of higher and more volatile oil prices persists. For investors and policymakers alike, the episode is a reminder that geopolitical risk can reassert itself quickly, with far-reaching implications for inflation, growth and financial markets.

References

- Financial Times, “Oil shortages are coming, and with them some difficult questions,” 15 April 2026

- Financial Times, “Falling Chinese oil imports ‘shield’ global market from higher prices,’ 4 June 2026

- The Wall Street Journal, “A rush to stockpile oil will keep prices higher for longer,” 9 June 2026