The International Monetary Fund (IMF) has recently updated its global outlook, offering a mixed picture of resilience and emerging fragility. While the global economy has held up better than feared in the face of recent shocks, the Fund has trimmed its growth expectations and raised its inflation projections, underscoring a more complicated macroeconomic backdrop.

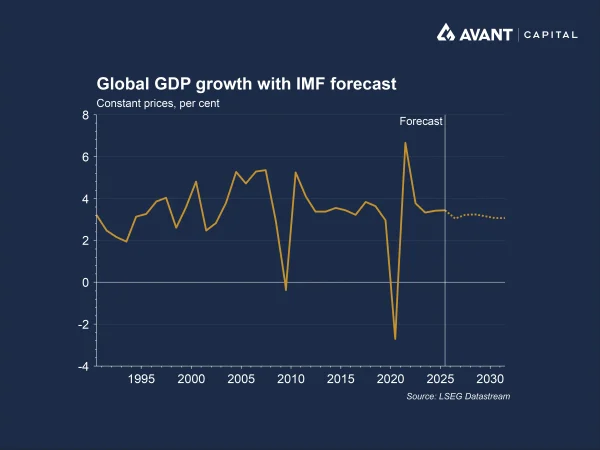

According to the IMF’s latest World Economic Outlook update, global growth is now projected to ease from 3.5% in 2025 to 3.0% in 2026, before recovering modestly to 3.4% in 2027. At the same time, inflation has been revised higher, with global price growth expected to rise to 4.7% this year, up from earlier projections, before easing gradually to 3.9% by 20271.

This reflects a key shift: after a period of steady disinflation since early 2024, the IMF now believes that progress on inflation has stalled. The global economy remains resilient, partly supported by strong activity in AI-related sectors, but this strength is uneven and comes with new sources of risk.

Why are geopolitical risks so critical?

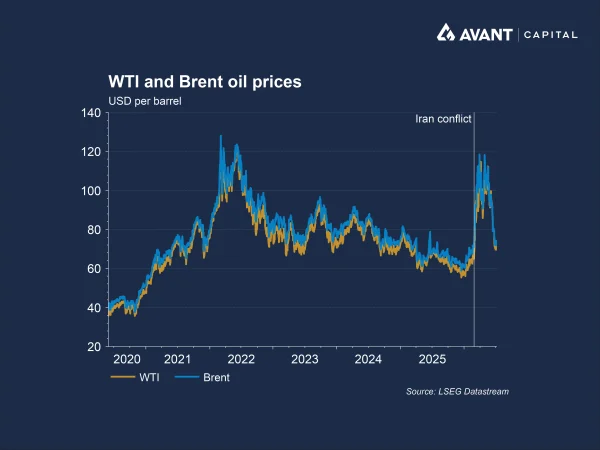

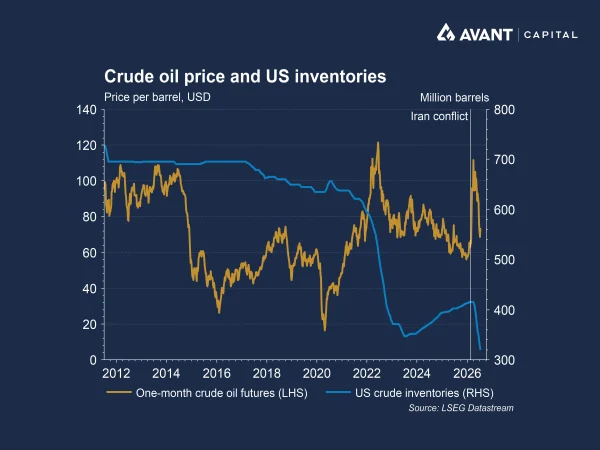

The most immediate risk flagged by the IMF centres on renewed tensions in the Middle East, particularly the potential escalation of conflict involving Iran. The breakdown of a ceasefire and renewed military strikes between the US and Iran have already begun to reverberate across markets.

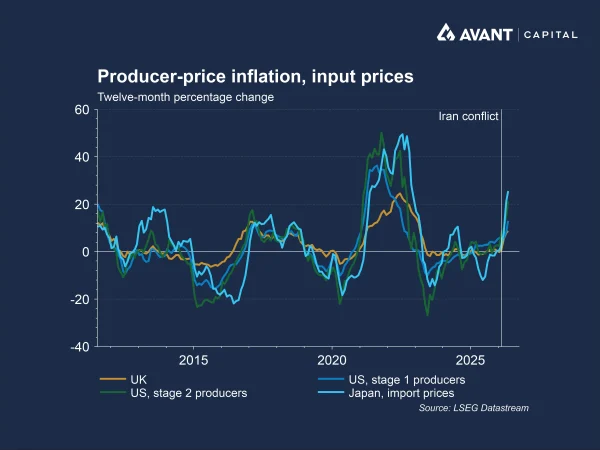

Energy markets have reacted swiftly. Brent crude prices have climbed sharply, with intra-day moves exceeding 5% as tensions escalated. The Strait of Hormuz, through which roughly one-fifth of global oil and gas supply previously flowed, has once again become a focal point, with disruptions to shipping and attacks on vessels raising concerns about supply constraints.

The IMF warns that any re-escalation could drive up commodity prices, worsen supply shortages, and add pressure to already stretched inventories, which are approaching “stress levels.” Crucially, these shocks extend beyond energy. Disruptions to fertiliser and food supply chains could amplify inflationary pressures, particularly for emerging economies. The interplay between geopolitics and inflation is therefore central to the current outlook.

What role is AI playing in the global growth story?

Artificial intelligence remains one of the most important drivers of the current economic outlook. On the one hand, AI investment has provided a meaningful boost to global growth, both in the United States and in export-oriented economies such as Taiwan, South Korea and parts of Southeast Asia.

On the other hand, concerns are mounting about the sustainability of this boom. The Bank for International Settlements (BIS) has warned that the current surge in AI investment could lead to an eventual “investment bust” if returns fail to meet expectations2.

The BIS highlights that hyperscalers, large cloud and technology companies such as Amazon, Microsoft and Google that invest heavily in data centres and computing infrastructure, are expected to invest over $US1 trillion between 2025 and 2026, a level of capital expenditure that may exceed what commercial returns can justify.

Financial markets are already showing signs of strain. Semiconductor stocks, which have been a key driver of broader market performance amid the AI boom, remain central to this trend. Analysts are forecasting 25% earnings growth for S&P 500 companies for the coming year, largely driven by AI, but concerns are growing that these expectations may be unrealistic3. Similarly, South Korean equities, closely tied to the AI chip supply chain, have entered a technical bear market, with the Kospi falling more than 20% from its peak in June4.

In this context, AI is both a growth engine and a potential source of downside risk.

Are central banks turning more hawkish again?

Rising inflation risks are reshaping the policy outlook, particularly for major central banks. Recent Federal Reserve minutes suggest a clear shift toward a more hawkish stance, with policymakers indicating that further rate increases may be necessary if inflation remains elevated. Market expectations have adjusted accordingly. Investors are now pricing in additional rate hikes across major economies, including the US, Eurozone and UK.

The drivers of this shift are multifaceted. Beyond energy costs, the Fed has identified AI-related investment, tariffs, and geopolitical tensions as overlapping sources of persistent inflation. This creates a challenging environment for policymakers, who must balance the risk of entrenched inflation against the potential for slowing growth. The IMF’s outlook reflects this tension, with policy uncertainty itself becoming a key risk factor.

What does the IMF outlook mean for Australia specifically?

The global themes identified by the IMF are also playing out in Australia, where the outlook has softened alongside persistent inflation pressures. The Fund has downgraded Australia’s growth forecast to 1.9% in 2026, placing it mid-pack among major economies and highlighting a broader trend of slowing momentum5.

At the same time, policymakers appear willing to tolerate weaker growth in order to bring inflation back under control. The Reserve Bank has signalled that higher unemployment and potentially further rate increases may be required if price pressures persist, underscoring the trade-off between growth and inflation.

Could financial markets be underestimating risks?

Despite growing risks, financial markets have remained relatively resilient, though there are signs this may be changing. Equity markets have been buoyed by strong earnings and AI-driven optimism, but warnings of valuation excesses are becoming more frequent.

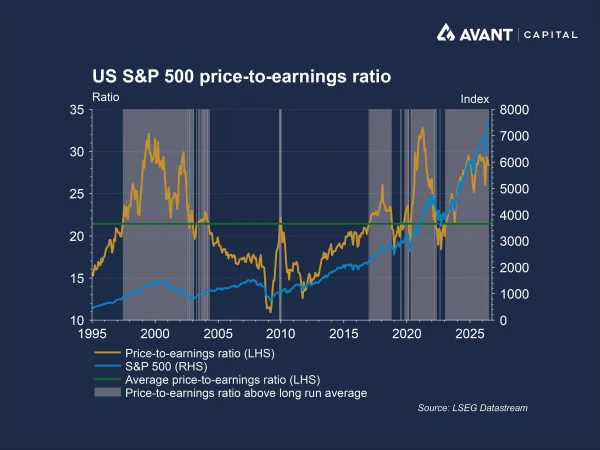

Some analysts argue that US equity valuations are approaching levels last seen during the dotcom bubble, with the S&P 500’s current price-to-earnings ratio significantly above long-run averages. At the same time, earnings themselves are running well above long-term trends, suggesting a dual risk of valuation and earnings compression.

The BIS echoes these concerns, noting that a sharp pullback in AI investment could trigger broader financial instability, particularly given the large volumes of debt issued to fund the current boom.

Taken together, these dynamics point to a market environment where optimism about growth could quickly give way to concerns about sustainability.

What does this mean for the global outlook?

The IMF’s latest update underscores a delicate balance in the global economy. Growth remains positive but subdued, inflation is proving more persistent than expected, and risks are increasingly skewed to the downside.

Geopolitical tensions, particularly around the Strait of Hormuz, have the potential to disrupt energy markets and reignite inflation. AI continues to support growth but introduces new financial vulnerabilities, while central banks are navigating a more complex policy environment.

Ultimately, the IMF’s message is one of cautious resilience. The global economy has adapted to recent shocks, but the margin for error is narrowing. As geopolitical, technological and financial forces converge, the outlook remains highly sensitive to developments on multiple fronts.

References

- Financial Times, “IMF warns inflation threat looms large over global economy,” 8 July 2026

- Financial Times, “AI ‘exuberance’ risks ending in lengthy investment bust, BIS warns,” 28 June 2026

- Financial Times, “Surging Wall Street profit forecasts fuel fears of ‘earnings bubble,’” 3 July 2026

- Financial Times, “South Korea falls into bear market as traders fret over AI chipmakers’ prospects,” 8 July 2026

- The Australian Financial Review, “IMF downgrades Australia’s economic growth,” 8 July 2026